1 Objective

The objective of this chapter is to give guidance on the manner in which the IPSAS financial statements would be presented and generated. To achieve this objective, this chapter provides an illustrative set of IPSAS model financial statements (MFS) for UN Volume I which sets out overall considerations for the presentation of financial statements, guidance for their structure, and minimum requirements for the content of financial statements prepared under IPSAS. Additional guidance on the recognition, measurement, and disclosure of specific transactions and other events are dealt with in other chapters of this finance manual. This chapter will also provide the process to automatically generate the tables to the financial statements and the notes using the Umoja Business Planning and Consolidation (BPC) program in order to produce the complete and final set of financial statements.

2 Summary of IPSAS Accounting Policies

2.1 Presentation of Financial Statements

Financial statements. The financial statements shall be prepared annually in United States dollars in accordance with the Financial Regulations and Rules of the United Nations (ST/SGB/2013/4), decisions of the appropriate legislative bodies and the International Public Sector Accounting Standards (Regulation 6.1).

Accrual basis accounting. Unless otherwise directed by the particular terms governing the operation of a trust fund or special account, all financial transactions shall be recorded in the accounts on an accrual basis in compliance with the International Public Sector Accounting Standards (Rule 106.3 of the Financial Regulations and Rules (ST/SGB/2013/4)).

The illustrative set of UN Volume I's financial statements included in this chapter is based on ST/IC/2013/36 of 31 December 2013 on the United Nations Policy Framework for the International Public Sector Accounting Standards. Although, the MFS attempts to create a realistic set of financial statements for UN Volume I, the disclosures in MFS should not be considered the only acceptable form of presentation. Alternative presentations to those proposed in this MFS may be equally acceptable if they comply with the specific disclosure requirements prescribed in IPSAS. The form and content of each UN Secretariat reporting entity's financial statements are the responsibility of each reporting entity.

These illustrative financial statements are not a substitute for professional judgment as to fairness of presentation. They do not cover all possible disclosures that IPSAS requires. For instance certain types of transaction and disclosure requirements may have been excluded, as they may not be relevant to the UN Volume I's operations.

A complete set of financial statements should include:

a. Statement of Financial Position;

b. Statement of Financial Performance;

c. Statement of Changes in Net Assets;

d. Statement of Cash Flows;

e. Statement of Comparison of Budget and Actual Amounts, on the basis of the budget; and

f. Notes to the financial statements comprising a summary of significant accounting policies and other explanatory notes.

Key policy guidance with regards to presentation of financial statements includes:

a. The UN shall use the current and non‐current classifications for assets and liabilities when preparing the statement of financial position;

b. The UN shall present, on the face of the statement of financial performance, a breakdown of expenses using a classification based on nature;

c. The UN shall present a statement of changes in net assets showing all the changes in net assets during that financial period by relevant groupings;

d. The UN shall present the statement of cash flows by applying indirect method for cash flows from operating activity and disclose investing and financing transactions that do not require the use of cash or cash equivalents;

e. Cash and cash equivalents not available for use by the reporting entity must be disclosed in the notes to the financial statements;

f. The UN continues to prepare the budgets on the same modified cash basis as prior to IPSAS adoption. Material variances between the final budget and actual amounts on modified cash basis requiring explanation will be at the level of 10% by budget section for Regular Budget and other approved budgets by section and 5% for Peacekeeping Operations at a Mission level; and

g. The financial statements should present an aggregated view of the reporting entity along with fund group reporting in the notes to the financial statements.

2.2 Preparation and Presentation of General Purpose Financial Reports

The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities (the Conceptual Framework) establishes and makes explicit the concepts that are to be applied in developing International Public Sector Accounting Standards (IPSASs) and Recommended Practice Guidelines (RPGs) applicable to the preparation and presentation of general purpose financial reports (GPFRs) of public sector entities. While the Conceptual Framework reflects a scope of financial reporting that is more comprehensive than that encompassed by financial statements, information presented in financial statements remains at the core of financial reporting.

The Conceptual Framework states that the objectives of financial reporting are to provide information about the entity that is useful to users of GPFRs for accountability purposes and for decision-making purposes. For the purposes of the Conceptual Framework, the primary users of GPFRs are service recipients and their representatives and resource providers and their representatives. While other parties may find the information provided by GPFRs useful, they are not the primary users of GPFRs. Therefore, GPFRs are not developed to specifically respond to their particular information needs of parties other than service recipients and resource providers.

The qualitative characteristics of information included in GPFRs are relevance, faithful representation, understandability, timeliness, comparability, and verifiability. Pervasive constraints on information included in GPFRs are materiality, cost-benefit, and achieving an appropriate balance between the qualitative characteristics. Each of the qualitative characteristics is integral to, and works with, the other characteristics to provide in GPFRs information useful for achieving the objectives of financial reporting. However, in practice, all qualitative characteristics may not be fully achieved, and a balance or trade-off between certain of them may be necessary.

2.3 Reference

For more details on the IPSAS requirements regarding presentation of financial statements, refer to:

· The UN IPSAS Policy Framework (ST/IC/2013/6) with emphasize on sections on IPSAS 1 Presentation of Financial Statements; IPSAS 2 Cash Flow Statements; and IPSAS 24 Presentation of Budget Information in Financial Statements.

· The Corporate Guidance on Reporting of Budget Information in Financial Statements, Segment Reporting and Presentation of Statement of Changes in Net Assets.

3 UN Volume I's Model Financial Statements

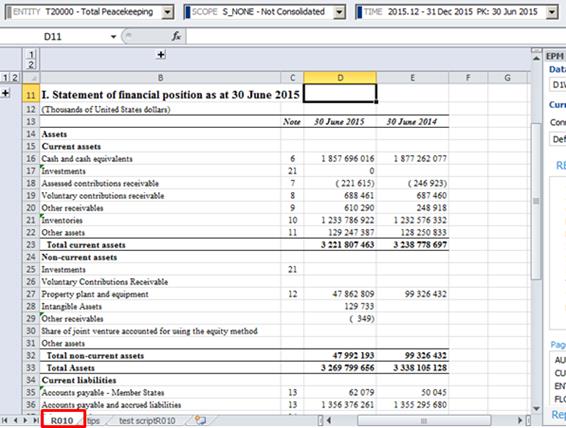

3.1 Statement I: Statement of Financial Position

|

(Thousands of United States dollars) |

|

|||

|

|

Note |

31 December 20X2 |

31 December 20X1 |

|

|

Assets |

|

|

|

|

|

Current assets |

|

|

|

|

|

Cash and cash equivalents |

7 |

|

|

|

|

Investments |

8 |

|

|

|

|

Assessed contributions receivable |

9 |

|

|

|

|

Voluntary contributions receivable |

10 |

|

|

|

|

Other receivables |

11 |

|

|

|

|

Inventories |

12 |

|

|

|

|

Other assets |

13 |

|

|

|

|

Total current assets |

|

|

|

|

|

Non-current assets |

|

|

|

|

|

Investments |

8 |

|

|

|

|

Voluntary contributions receivable |

10 |

|

|

|

|

Property, plant and equipment |

15 |

|

|

|

|

Intangible assets |

16 |

|

|

|

|

Share of joint ventures accounted for using the equity method |

24 |

|

|

|

|

Other assets |

13 |

|

|

|

|

Total non-current assets |

|

|

|

|

|

Total Assets |

|

|

|

|

|

Liabilities |

|

|

|

|

|

Current liabilities |

|

|

|

|

|

Accounts payable and accrued liabilities |

17 |

|

|

|

|

Advance receipts |

18 |

|

|

|

|

Employee benefit liabilities |

19 |

|

|

|

|

Provisions |

20 |

|

|

|

|

Tax equalization liability |

21 |

|

|

|

|

Other liabilities |

22 |

|

|

|

|

Total current liabilities |

|

|

|

|

|

Non-current liabilities |

|

|

|

|

|

Advance receipts |

18 |

|

|

|

|

Employee benefit liabilities |

19 |

|

|

|

|

Provisions |

20 |

|

|

|

|

Share of joint ventures accounted for using the equity method |

24 |

|

|

|

|

Other liabilities |

22 |

|

|

|

|

Total non-current liabilities |

|

|

|

|

|

Total liabilities |

|

|

|

|

|

Net of total assets and total liabilities |

|

|

|

|

|

|

|

|

|

|

|

Net assets |

|

|

|

|

|

Accumulated surplus/(deficit) |

25 |

|

|

|

|

Reserves |

25 |

|

|

|

|

Total net assets |

|

|

|

|

The accompanying notes to the financial statements are an integral part of these financial statements.

3.2 Statement II: Statement of Financial Performance

|

(Thousands of United States dollars) |

|||

|

|

Note |

20X2 |

20X1 |

|

Revenue |

|

|

|

|

Assessed contributions |

26 |

|

|

|

Voluntary contributions |

26 |

|

|

|

Other transfers and allocations |

26 |

|

|

|

Investment revenue |

30 |

|

|

|

Contributions for self-insurance funds |

28 |

|

|

|

Other revenue |

27 |

|

|

|

Total revenue |

|

|

|

|

Expenses |

|||

|

Employee salaries, allowances and benefits |

29 |

|

|

|

Non-employee compensation and allowances |

|

|

|

|

Grants and other transfers |

29 |

|

|

|

Supplies and consumables |

|

|

|

|

Depreciation and amortization |

15, 16 |

|

|

|

Impairment |

15 |

|

|

|

Travel |

|

|

|

|

Other operating expenses |

29 |

|

|

|

Self-insurance claims and expenses |

28 |

|

|

|

Finance costs |

33 |

|

|

|

Contributions to and share of deficit of joint ventures accounted for on an equity basis |

24 |

|

|

|

Other expenses |

|

|

|

|

[Add material items as separate line item] |

|

|

|

|

Total expenses |

|

|

|

|

Surplus / (deficit) for the year |

|

|

|

The accompanying notes to the financial statements are an integral part of these financial statements.

3.3 Statement III: Statement of Changes in Net Assets

|

(Thousands of United States dollars) |

||

|

|

|

Net assets |

|

Net assets as at 31 December 20X0 |

|

|

|

Changes in net assets |

|

|

|

Actuarial gains / (losses) on employee benefit liabilities (note 19) |

|

|

|

Transfers of funds to / from other organizations/entities |

|

|

|

Share of changes recognized by joint ventures directly in net assets (note 24) |

|

|

|

Other adjustments to net assets |

|

|

|

Surplus / (deficit) for the year |

|

|

|

[Add additional items recognized in net assets] |

|

|

|

Total changes in net assets |

|

|

|

Net assets as at 31 December 20X1 (note 25) |

|

|

|

Prior-period adjustments (note 4) |

|

|

|

Restated net assets as at 31 December 20X1 (note 25) |

|

|

|

Changes in net assets |

|

|

|

Actuarial gains / (losses) on employee benefit liabilities (note 19) |

|

|

|

Transfers of funds to / from other organizations/entities |

|

|

|

Share of changes recognized by joint ventures directly in net assets (note 24) |

|

|

|

Other adjustments to net assets |

|

|

|

Surplus / (deficit) for the year |

|

|

|

[Add additional items recognized in Net assets] |

|

|

|

Total changes in net assets |

|

|

|

Net assets as at 31 December 20X2 (note 25) |

|

|

The accompanying notes to the financial statements are an integral part of these financial statements.

3.4 Statement IV: Statement of Cash Flows

|

(Thousands of United States dollars) |

|||

|

|

Note |

20X2 |

20X1 |

|

Cash flows from operating activities |

|

|

|

|

Surplus / (deficit) for the year |

|

|

|

|

Non-cash movements |

|

|

|

|

Depreciation and amortization |

15, 16 |

|

|

|

Impairment of property, plant and equipment and intangible assets |

15, 16 |

|

|

|

Impairment of inventory |

12 |

|

|

|

Increase / (decrease) in allowance for doubtful receivables |

9, 10, 11 |

|

|

|

Net loss /(gain) on disposal of property, plant and equipment and inventory |

|

|

|

|

Investment revenue presented in net receipts from cash pool investments |

30 |

|

|

|

Current service cost and interest cost of employee benefit liabilities |

19 |

|

|

|

Donation of assets |

26 |

|

|

|

Net deficit / (surplus) on joint ventures |

24 |

|

|

|

[Additional non-cash items to be added] |

|

|

|

|

Changes in assets |

|

|

|

|

(Increase) / decrease in assessed contributions receivable |

9 |

|

|

|

(Increase) / decrease in voluntary contributions receivable |

10 |

|

|

|

(Increase) / decrease in other receivables |

11 |

|

|

|

(Increase) / decrease in inventories |

12 |

|

|

|

(Increase) / decrease in other assets |

13 |

|

|

|

(Increase) / decrease in share of joint venture asset/liability accounted for using the equity method |

24 |

|

|

|

Changes in liabilities |

|

|

|

|

Increase / (decrease) in accounts payable and accrued liabilities |

17 |

|

|

|

Increase / (decrease) in advance receipts |

18 |

|

|

|

Increase / (decrease) in employee benefit liabilities |

19 |

|

|

|

Increase / (decrease) in provisions |

20 |

|

|

|

Increase / (decrease) in tax equalization fund liability |

21 |

|

|

|

Increase / (decrease) in other liabilities |

22 |

|

|

|

Increase / (decrease) in share of joint venture asset/liability accounted for using the equity method |

24 |

|

|

|

Net cash flows from operating activities |

|

|

|

|

Cash flows from investing activities |

|

|

|

|

Net changes in cash pool investments |

30 |

|

|

|

Acquisitions of property, plant and equipment |

15, 26 |

|

|

|

Proceeds from disposal of property, plant and equipment |

15 |

|

|

|

Acquisitions of intangible assets |

16, 26 |

|

|

|

Donation of intangible assets |

|

|

|

|

Issuance of loans receivable |

|

|

|

|

Proceeds from repayment of loans receivable |

|

|

|

|

[Additional investing activities to be added] |

|

|

|

|

Net cash flows from investing activities |

|

|

|

|

Cash flows from financing activities |

|

|

|

|

Proceeds from borrowings |

|

|

|

|

Repayment of borrowings |

|

|

|

|

[Additional financing activities to be added] |

|

|

|

|

Net cash flows from financing activities |

|

|

|

|

Net increase /(decrease) in cash and cash equivalents |

|

|

|

|

Cash and cash equivalents - beginning of year |

|

|

|

|

Exchange gains /(losses) on cash and cash equivalents |

|

|

|

|

Cash and cash equivalents - end of year |

7 |

|

|

Note:

· Investing and financing non-cash transactions should be disclosed by way of note to cash flow statement.

· Interest received and paid shall each be disclosed separately.

The accompanying notes to the financial statements are an integral part of these financial statements

3.5 Statement V: Statement of Comparison of Budget and Actual Amounts

|

(Thousands of United States dollars) |

||||||

|

|

Publicly available budget |

Actual annual expenditure (budget basis) |

Difference (percentage) |

|||

|

Original biennial |

Final biennial |

Original annual |

Final annual |

|||

|

Regular budget |

|

|

|

|

|

|

|

Overall policymaking, direction and coordination |

|

|

|

|

|

|

|

Political affairs |

|

|

|

|

|

|

|

International justice and law |

|

|

|

|

|

|

|

International cooperation for development |

|

|

|

|

|

|

|

Regional cooperation for development |

|

|

|

|

|

|

|

Human rights and humanitarian affairs |

|

|

|

|

|

|

|

Public information |

|

|

|

|

|

|

|

Common support services |

|

|

|

|

|

|

|

Internal oversight |

|

|

|

|

|

|

|

Jointly financed administrative activities and special expenses |

|

|

|

|

|

|

|

Capital expenditures |

|

|

|

|

|

|

|

Security and safety |

|

|

|

|

|

|

|

Development account |

|

|

|

|

|

|

|

Staff assessment |

|

|

|

|

|

|

|

Subtotal, regular budget |

|

|

|

|

|

|

|

Other publicly available budgets |

|

|

|

|

|

|

|

Capital master plan |

|

|

|

|

|

|

|

[Add other available budgets] |

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

The accompanying notes to the financial statements are an integral part of these financial statements.

4 Notes to the Financial Statements

4.1 Note 1: Reporting entity

The United Nations and its activities

1. The United Nations is an international organization founded in 1945 after the Second World War. The Charter of the United Nations, which was signed on 26 June 1945 and became effective on 24 October 1945, sets out the primary objectives of the United Nations as follows:

(a). The maintenance of international peace and security;

(b). The promotion of international economic and social progress and development programmes;

(c). The universal observance of human rights;

(d). The administration of international justice and law.

2. These objectives are implemented through the major organs of the United Nations, as follows:

(a). The General Assembly focuses on a wide range of political, economic and social issues, as well as financial and administrative aspects of the Organization;

(b). The Security Council is responsible for various aspects of peacekeeping and peacebuilding, including efforts to resolve conflicts, restore democracy, promote disarmament, provide electoral assistance, facilitate post-conflict peacebuilding, engage in humanitarian activities to ensure the survival of groups deprived of basic needs, and oversee the prosecution of persons responsible for serious violations of international humanitarian law;

(c). The Economic and Social Council plays a particular role in economic and social development, including a major oversight role in the efforts of other organizations of the United Nations system to address international economic, social and health problems;

(d). The International Court of Justice has jurisdiction over disputes between Member States brought before it for advisory opinions or binding resolutions.

3. The United Nations has its headquarters in New York. It has major offices in Geneva, Vienna and Nairobi, and peacekeeping and political missions, economic commissions, tribunals, training institutes and other centres around the world.

Operations of the United Nations as reported in volume I

4. The present financial statements relate to the operations of the United Nations as reported in Volume I, a separate financial reporting entity of the United Nations for the purposes of IPSAS-compliant reporting. The operations of the United Nations, as reported in volume I, comprise the core operations of the Secretariat and are under the direction of the General Assembly in its role as lead organ for the financial and administrative aspects of the United Nations. The core operations of the Secretariat are funded by the regular budget, which has a unique scale of assessments and budgetary process, by trust funds established by the Assembly or the Secretary-General, which supplement the activities of the regular budget, or by special accounts or funds established to facilitate mandate implementation by the Secretary-General in his/her role as Chief Administrative Officer of the United Nations.

5. The reporting entity - the operations of the United Nations as reported in volume I - is regarded as an autonomous reporting entity that, owing to the uniqueness of the governance and budgetary process of each of the reporting entities of the United Nations, neither controls nor is controlled by any other United Nations financial reporting entity. Therefore, consolidation is not applicable to the operations of the United Nations and its financial statements include only its activities as reported in volume I.

6. However, given the existence of a joint venture between the United Nations and the World Trade Organization for the International Trade Centre (ITC) [Add other organizations where applicable], and the significant influence of the United Nations over the operations of ITC [Add other organizations where applicable], the United Nations has accounted for its investment in ITC [Add other organizations where applicable] using the equity method of accounting. The Organization participates in a number of jointly financed activities with other United Nations system organizations. The Organization's share of those activities is also included in the financial statements using the equity method.

7. The United Nations regular budget includes an assessed portion of the budget of other United Nations reporting entities, comprising the United Nations Environment Programme, the United Nations Office on Drugs and Crime, the United Nations Human Settlements Programme, the United Nations Relief and Works Agency for Palestine Refugees in the Near East, the Office of the United Nations High Commissioner for Refugees and the United Nations Entity for Gender Equality and the Empowerment of Women [Add other organizations where applicable]. Those amounts are accounted for as grants in volume I.

8. The financial statements comprise activities managed through various funds, as follows:

(a). General Fund and related funds. The General Fund relates to regular budget activities and related funds consist of the Special Account and the Working Capital Fund;

(b). General trust funds. General trust funds are established to record the receipt of voluntary contributions to support various activities, including emergency assistance, political, economic and social development and humanitarian and human rights activities and those that relate to security issues, international justice and law, public information and support services;

(c). Capital funds. Capital funds include capital assets and construction-in-progress funds at various locations worldwide. [Add major projects included under these funds];

(d). Tax Equalization Fund. The Tax Equalization Fund was established to equalize the net pay of all staff members, whatever their national tax obligations;

(e). End-of-service and post-retirement benefits. Such funds were established to account for end-of-service liabilities in respect of benefits payable to staff separating from service and comprise after-service health insurance, repatriation benefits and unused annual leave;

(f). Other funds. These comprise self-insurance funds; special accounts for administrative cost recoveries; common support services; conferences and conventions; special multi-year funds accounting for supplementary development activities; and other funds.

4.2 Note 2: Basis of preparation and authorization for issue

Basis of preparation

9. In accordance with the Financial Regulations and Rules of the United Nations, these financial statements have been prepared on an accrual basis in accordance with the International Public Sector Accounting Standards (IPSAS). They have been prepared on a going-concern basis, and the accounting policies have been applied consistently in their preparation and presentation. In accordance with the requirements of IPSAS, the financial statements, which present fairly the assets, liabilities, revenue and expenses of the Organization, consist of the following:

(a). Statement of financial position (statement I);

(b). Statement of financial performance (statement II);

(c). Statement of changes in net assets (statement III);

(d). Statement of cash flows (using the indirect method) (statement IV);

(e). Statement of comparison of budget and actual amounts (statement V);

(f). Notes to the financial statements comprising a summary of significant accounting policies and other explanatory notes;

(g). Comparative information in respect of all amounts presented in the financial statements indicated in (a) to (e) above and, where relevant, comparative information for narrative and descriptive information presented in the notes to these financial statements.

Going concern

10. The going concern assertion is based on the approval by the General Assembly of the regular budget appropriations for the biennium [ ], the positive historical trend of collection of assessed and voluntary contributions over the past years and the fact that the Assembly has taken no decision to cease the operations of the United Nations.

Authorization for issue

11. These financial statements are certified by the Controller and approved by the Secretary-General. In accordance with financial regulation 6.2, the Secretary-General shall transmit these financial statements as at 31 December 20X2 to the Board of Auditors by 31 March 20X3. In accordance with financial regulation 7.12, the reports of the Board of Auditors are to be transmitted to the General Assembly through the Advisory Committee on Administrative and Budgetary Questions, together with the audited financial statements authorized for issue on [ ] 20X3.

Note: If any another body has the power to amend the financial statements after issuance, that fact should be disclosed.

Measurement basis

12. These financial statements are prepared using the historical-cost convention, except for real estate assets that are recorded at depreciated replacement cost and financial assets recorded at fair value through surplus or deficit.

Functional and presentation currency

13. The functional currency and the presentation currency of the Organization is the United States dollar. The financial statements are expressed in thousands of United States dollars unless otherwise stated.

14. Transactions in currencies other than the functional currency (foreign currencies) are translated into United States dollars at the United Nations operational rate of exchange at the date of the transaction. The United Nations operational rates of exchange approximate the spot rates prevailing at the dates of the transactions. At year end, monetary assets and liabilities denominated in foreign currencies are translated at the United Nations operational rates of exchange. Non-monetary foreign currency denominated items that are measured at fair value are translated at the United Nations operational rates of exchange at the date on which the fair value was determined. Non-monetary items measured at historical cost in a foreign currency are not translated at year end.

15. Foreign exchange gains and losses resulting from the settlement of foreign currency transactions and from the translation of monetary assets and liabilities denominated in foreign currencies at year-end exchange rates are recognized in the statement of financial performance on a net basis.

Materiality and use of judgment and estimation

16. Materiality is central to the preparation and presentation of the Organization's financial statements and its materiality framework provides a systematic method in guiding accounting decisions relating to presentation, disclosure, aggregation, offsetting and retrospective versus prospective application of changes in accounting policies. In general, an item is considered material if its omission or its aggregation would have an impact on the conclusions or decisions of the users of the financial statements.

17. Preparing financial statements in accordance with IPSAS requires use of estimates, judgments and assumptions in the selection and application of accounting policies and in the reported amounts of certain assets, liabilities, revenues and expenses.

18. Accounting estimates and underlying assumptions are reviewed on an ongoing basis and revisions to estimates are recognized in the year in which the estimates are revised and in any future year affected. Significant estimates and assumptions that may result in material adjustments in future years include: actuarial measurement of employee benefits; selection of useful lives and the depreciation/amortization methods for property, plant and equipment/intangible assets; impairment of assets; classification of financial instruments; valuation of inventory; inflation and discount rates used in the calculation of the present value of provisions and classification of contingent assets/liabilities.

International Public Sector Accounting Standards transitional provisions

19. As permitted on first time adoption of IPSAS, the following transitional provisions are applied: [Add relevant transitional provisions applied on adoption of IPSAS]

Future accounting pronouncements

20. The progress and impact of the following significant future IPSAS Board accounting pronouncements on the Organization's financial statements continues to be monitored [Insert relevant IPSASB pronouncements with explanations].

4.3 Note 3: Significant accounting policies

Financial assets classification

21. The classification of financial assets depends primarily on the purpose for which the financial assets are acquired. The Organization classifies its financial assets in one of the categories shown below at initial recognition and re-evaluates the classification at each reporting date.

|

Classification |

Financial assets |

|

Fair value through surplus or deficit |

Investments in cash pools, [Add additional items if required] |

|

Loans and receivables |

Cash and cash equivalents and receivables [Add additional items if required] |

Note: If any financial assets are classified as Held to maturity or Available for sale, appropriate disclosures should be included in the financial statements.

22. All financial assets are initially measured at fair value. The Organization initially recognizes financial assets classified as loans and receivables on the date on which they originated. All other financial assets are recognized initially on the trade date, which is the date on which the Organization becomes party to the contractual provisions of the instrument.

23. Financial assets with maturities in excess of 12 months at the reporting date are categorized as non-current assets in the financial statements. Assets denominated in foreign currencies are translated into United States dollars at the United Nations operational rates of exchange prevailing at the reporting date, with net gains or losses recognized in surplus or deficit in the statement of financial performance.

24. Financial assets at fair value through surplus or deficit are those that have been designated in this category at initial recognition, are held for trading or are acquired principally for the purpose of selling in the short term. These assets are measured at fair value at each reporting date, and any gains or losses arising from changes in the fair value are presented in the statement of financial performance in the year in which they arise.

25. Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are initially recorded at fair value, plus transaction costs and are subsequently reported at amortized cost calculated using the effective interest method. Interest revenue is recognized on a time proportion basis using the effective interest rate method on the respective financial asset.

26. Financial assets are assessed at each reporting date to determine whether there is objective evidence of impairment. Evidence of impairment includes default or delinquency of the counterparty or permanent reduction in the value of the asset. Impairment losses are recognized in the statement of financial performance in the year in which they arise.

27. Financial assets are derecognized when the rights to receive cash flows have expired or have been transferred and the Organization has transferred substantially all risks and rewards of the financial asset. Financial assets and liabilities are offset and the net amount is reported in the statement of financial position when there is a legally enforceable right to offset the recognized amounts and there is an intention to settle on a net basis or realize the asset and settle the liability simultaneously.

Investment in cash pools

28. The United Nations Treasury invests funds pooled from Secretariat entities and other participating entities. These pooled funds are combined in two internally managed cash pools. Participation in a cash pool implies sharing the risk and returns on investments with the other participants. Given that the funds are commingled and invested on a pool basis, each participant is exposed to the overall risk of the investment portfolio to the extent of the amount of cash invested.

29. The Organization's investments in the cash pools are included as part of cash and cash equivalents, short-term investments and long-term investments in the statement of financial position depending on the maturity period of the investment.

Cash and cash equivalents

30. Cash and cash equivalents comprise cash at bank and on hand, and short-term, highly liquid investments with a maturity of three months or less from the date of acquisition [Add other financial instruments classified as cash equivalents if applicable].

Receivables from non-exchange transactions: contributions receivable

31. Contributions receivable represent uncollected revenue from assessed and voluntary contributions committed to the Organization by Member States, non-member States and other donors on the basis of enforceable agreements. These non-exchange receivables are stated at nominal value, less impairment for estimated irrecoverable amounts, the allowance for doubtful receivables. Voluntary contributions receivable are subject to an allowance for doubtful receivables on the same basis as other receivables. For assessed contributions receivable, the allowance for doubtful receivables is calculated as follows; [Please refer to the UN IPSAS Policy Framework for the latest guidance of the calculations].

Receivables from exchange transactions: other receivables

32. Other receivables include amounts receivable for goods or services provided to other entities, amounts receivable for leased-out assets and receivables from staff. Receivables from other United Nations reporting entities are also included in this category. Material balances of other receivables and voluntary contributions receivable are subject to specific review and an allowance for doubtful receivables is assessed on the basis of recoverability and ageing accordingly.

Note: Add other significant line items included in other receivables i.e. inter fund balances and update policy if receivables are discounted.

Investments accounted for using the equity method

33. The equity method initially records an interest in jointly controlled entity at cost and is adjusted thereafter for the post-acquisition changes in the Organization's share of net assets. The Organization's share of the surplus or deficit of the investee is recognized in the statement of financial performance. The interest is recorded as a non-current asset unless there is a net liability position, in which case it is recorded as a non-current liability.

Other assets

34. Other assets include education grant advances and prepayments that are recorded as an asset until goods are delivered or services are rendered by the other party, at which point the expense is recognized.

Inventories

35. Inventory balances are recognized as current assets and include the categories set out below:

|

Categories |

Subcategories |

|

Held for sale or external distribution |

Books and publications, stamps |

|

Raw materials and work in progress associated with items held for sale or external distribution |

Construction materials/supplies, work in progress |

|

Strategic reserves |

Fuel reserves, bottled water and rations reserves |

|

Consumables and supplies |

Material holdings of consumables and supplies, including spare parts and medicines |

36. The cost of inventory in stock is determined using the average price cost basis. The cost of inventories includes the cost of purchase plus other costs incurred in bringing the items to the destination and condition for use. Inventory acquired through non-exchange transactions, i.e. donated goods, are measured at fair value at the date of acquisition. Inventories held for sale are valued at the lower of cost and net realizable value. Inventories held for distribution at no or nominal charge or for consumption in the production of goods or services are valued at the lower of cost and current replacement cost.

37. The carrying amount of inventories is expensed when inventories are sold, exchanged, distributed externally or consumed by the Organization. Net realizable value is the net amount that is expected to be realized from the sale of inventories in the ordinary course of operations. Current replacement cost is the estimated cost that would be incurred to acquire the asset.

38. Holdings of consumables and supplies for internal consumption are capitalized in the statement of financial position only when material. Such inventories are valued by the periodic weighted average of the moving average methods based on records available in the inventory management systems, such as Galileo and Umoja, which are validated through the use of thresholds, cycle counts and enhanced internal controls. Valuations are subject to impairment review, which takes into consideration the variances between moving average price valuation and current replacement cost, as well as slow-moving and obsolete items.

39. Inventories are subject to physical verification based on value and risk as assessed by management. Valuations are net of write-downs from cost to current replacement cost/net realizable value, which are recognized in the statement of financial performance.

Heritage assets

40. Heritage assets are not recognized in the financial statements, but significant heritage assets transactions are disclosed in the notes thereto.

Property, plant and equipment

41. Property, plant and equipment are classified into different groups, based on their nature, functions, useful lives and valuation methodologies, as: vehicles, communications and information technology equipment; machinery and equipment; furniture and fixtures; and real estate assets (land, buildings, leasehold improvements, infrastructure and assets under construction). Recognition of property, plant and equipment is as follows:

(a). Property, plant and equipment are capitalized when their cost per unit is greater than or equal to the threshold of USD 20,000, or USD 100,000 for leasehold improvements and self-constructed assets. A lower threshold of USD 5,000 applies to five commodity groups: vehicles; prefabricated buildings; satellite communication systems; generators; and network equipment;

(b). All property, plant and equipment, other than real estate assets, are stated at historical cost, less accumulated depreciation and accumulated impairment losses. Historical cost comprises the purchase price, any costs directly attributable to bringing the asset to its location and condition and the initial estimate of dismantling and site restoration costs;

(c). Owing to the absence of historical cost information, buildings and infrastructure real estate assets were initially recognized at fair value using a depreciated replacement cost methodology for initial IPSAS implementation. The method involves calculating the cost per unit of measurement, for example cost per square metre, by collecting construction cost data, utilizing in-house cost data (where available) or using external cost estimators for each catalogue of real estate assets and multiplying that unit cost by the external area of the asset to obtain the gross replacement cost. Depreciation allowance deductions from the gross replacement cost to account for physical, functional and economic use of the assets have been made to determine the depreciated replacement cost of the assets. With the exception of real estate assets located in the special political missions, any subsequent real estate additions are recognized at historical cost;

(d). With regard to property, plant and equipment acquired at nil or nominal cost including donated assets, the fair value at the date of acquisition is deemed to be the cost to acquire equivalent assets.

42. Property, plant and equipment are depreciated over their estimated useful lives using the straight-line method up to their residual value, except for land and assets under construction, which are not subject to depreciation. Given that not all components of a building have the same useful lives or the same maintenance, upgrade or replacement schedules, significant components of owned buildings are depreciated using the components approach. Depreciation begins in the month in which the Organization gains control over an asset in accordance with international commercial terms and no depreciation is charged in the month of retirement or disposal of PP&E. Given the expected pattern of usage of property, plant and equipment, the residual value is nil unless residual value is likely to be significant. The estimated useful lives of property, plant and equipment classes are set out below.

|

Class |

Subclass |

Estimated useful life |

|

Communications and information technology equipment |

Information technology equipment |

4 years |

|

Communication and audiovisual equipment |

7 years |

|

|

Vehicles |

Light-wheeled vehicles |

6 years |

|

|

Heavy-wheeled and engineering support vehicles |

12 years |

|

|

Specialized vehicles, trailers and attachments |

6 to 12 years |

|

|

Marine vessels |

10 years |

|

Machinery and equipment |

Light engineering and construction equipment |

5 years |

|

Medical equipment |

5 years |

|

|

|

Security and safety equipment |

5 years |

|

|

Mine detection and clearing equipment |

5 years |

|

|

Accommodation and refrigeration equipment |

6 years |

|

|

Water treatment and fuel distribution equipment |

7 years |

|

|

Transportation equipment |

7 years |

|

|

Heavy engineering and construction equipment |

12 years |

|

|

Printing and publishing equipment |

20 years |

|

Furniture and fixtures |

Library reference material |

3 years |

|

Office equipment |

4 years |

|

|

|

Fixtures and fittings |

7 years |

|

|

Furniture |

10 years |

|

Buildings |

Temporary and mobile buildings |

7 years |

|

|

Fixed buildings, depending on the type |

25, 40 or 50 years |

|

|

Major exterior, roofing, interior and services/utilities components, where component approach is utilized |

20 to 50 years |

|

|

Finance lease or donated right-to-use buildings |

Shorter of term of arrangement or life of building |

|

Infrastructure assets |

Telecommunications, energy, protection, transport, waste and water management, recreation, landscaping |

Up to 50 years |

|

Leasehold improvements |

Fixtures, fittings and minor construction work |

Shorter of lease term or 5 years |

43. Where there is a material cost value of fully depreciated assets that are still in use, adjustments to accumulated depreciation are incorporated into the financial statements to reflect a residual value of 10 per cent of historical cost based on an analysis of the classes and useful lives of the fully depreciated assets.

44. The Organization chose the cost model for measurement of property, plant and equipment after initial recognition instead of the revaluation model. Costs incurred subsequent to initial acquisition are capitalized only when it is probable that future economic benefits or service potential associated with the item will flow to the Organization and the subsequent cost exceeds the threshold for initial recognition. Repairs and maintenance are expensed in the statement of financial performance in the year in which they are incurred.

45. A gain or loss resulting from the disposal or transfer of property, plant and equipment arises when proceeds from disposal or transfer differ from its carrying amount. Those gains or losses are recognized in the statement of financial performance as part of other revenue or other expenses.

46. Impairment assessments are conducted during annual physical verification procedures and when events or changes in circumstance indicate that carrying amounts may not be recoverable. Land, buildings and infrastructure assets with a year-end net-book-value greater than USD 500,000 per unit are reviewed for impairment at each reporting date. The equivalent threshold for other property, plant and equipment items (excluding assets under construction and leasehold improvements) is USD 25,000.

Intangible assets

47. Intangible assets are carried at cost less accumulated amortization and accumulated impairment loss. For intangible assets acquired at nil or nominal cost, including donated assets, the fair value at the date of acquisition is deemed to be the cost of the asset. The thresholds for recognition are USD 100,000 per unit for internally generated intangible assets and USD 20,000 per unit for externally acquired intangible assets.

48. Acquired computer software licences are capitalized on the basis of costs incurred to acquire and bring into use the specific software. Development costs that are directly associated with the development of software for use by the Organization are capitalized as an intangible asset. Directly associated costs include software development employee costs, consultants costs and other applicable overhead costs.

49. Intangible assets with finite useful lives are amortized on a straight-line method, starting from the month of acquisition or when they become operational. The useful lives of major classes of intangible assets have been estimated as shown below.

|

Class |

Range of estimated useful life |

|

Licenses and rights |

2-6 years (period of license / right) |

|

Software acquired externally |

3-10 years |

|

Software internally developed |

3-10 years |

|

Copyrights |

3-10 years |

|

Assets under development |

Not amortized |

|

Other intangible assets |

[Name and life to be added if necessary based on facts and circumstances] |

50. Annual impairment reviews of intangible assets are conducted where assets are under development or have an indefinite useful life. Other intangible assets are subject to impairment review only when indicators of impairment are identified.

Financial liabilities: classification

51. Financial liabilities are classified as 'other financial liabilities'. They include accounts payable, transfers payable, unspent funds held for future refunds and other liabilities such as balances payable to other United Nations system reporting entities. Note: Add important line items based on facts and circumstances.

52. Financial liabilities classified as other financial liabilities are initially recognized at fair value and subsequently measured at amortized cost. Financial liabilities with a duration of less than 12 months are recognized at their nominal value. The Organization re-evaluates the classification of financial liabilities at each reporting date and derecognizes financial liabilities when its contractual obligations are discharged, waived, cancelled or expired.

Financial liabilities: accounts payable and accrued liabilities

53. Accounts payable and accrued liabilities arise from the purchase of goods and services that have been received but not paid for at the reporting date. Payables are recognized and subsequently measured at their nominal value because they are generally due within 12 months.

Advance receipts and other liabilities

54. Advance receipts and other liabilities consist of payments received in advance relating to exchange transactions, liabilities for conditional funding arrangements and other deferred revenue.

Leases

The Organization as 'lessee'

55. Leases of property, plant and equipment where the Organization has substantially all the risks and rewards of ownership are classified as finance leases. Finance leases are capitalized at the start of the lease at the lower of fair value or the present value of the minimum lease payments. The rental obligation, net of finance charges, is reported as a liability in the statement of financial position. Assets acquired under finance leases are depreciated in accordance with the property, plant and equipment policies. The interest element of the lease payment is charged to the statement of financial performance as an expense over the lease term on the basis of the effective interest rate method.

56. Leases where all of the risks and rewards of ownership are not substantially transferred to the Organization are classified as operating leases. Payments made under operating leases are charged to the statement of financial performance as an expense on a straight-line basis over the term of the lease.

The Organization as 'lessor'

57. The Organization often leases out assets under operating leases. Leased-out assets are reported under property, plant and equipment, and lease revenue is recognized in the statement of financial performance over the term of the lease on a straight-line basis.

Donated right-to-use

58. Land, buildings, infrastructure assets, machinery and equipment is frequently granted to the Organization, primarily by host Governments at nil or nominal cost, through donated right-to-use arrangements. These arrangements are accounted for as operating leases or finance leases depending on whether an assessment of the agreement indicates that control over the underlying asset is transferred to the Organization.

59. Where a donated right-to-use arrangement is treated as an operating lease, an expense and corresponding revenue equal to the annual rental value of the asset or similar property are recognized in the financial statements. Where a donated right-to-use arrangement is treated as a finance lease (principally with a lease term of over 35 years for premises), the fair market value of the property is capitalized and depreciated over the shorter of the useful life of the property or the term of the arrangement. In addition, a liability for the same amount is recognized, which is progressively recognized as revenue over the lease term. Donated right-to-use land arrangements are accounted for as operating leases where the Organization does not have exclusive control over the land and/or title to the land is transferred under restricted deeds.

60. Where title to land is transferred to the Organization without restrictions, the land is accounted for as donated property, plant and equipment and recognized at fair value at the acquisition date.

61. The threshold for the recognition of revenue and expense is a yearly rental value equivalent of USD 20,000 per unit for donated right-to-use premises and USD 5,000 per unit for machinery and equipment.

Employee benefits

62. Employees comprise staff members, as described under Article 97 of the Charter of the United Nations, whose employment and contractual relationship with the Organization are defined by a letter of appointment subject to regulations promulgated by the General Assembly pursuant to Article 101, paragraph 1, of the Charter.

63. Employee benefits are classified into short-term benefits, long-term benefits, post-employment benefits and termination benefits.

Short-term employee benefits

64. Short-term employee benefits are employee benefits (other than termination benefits) that are payable within 12 months after the end of the year in which the employee renders the related services. Short-term employee benefits comprise first-time employee benefits (assignment grants), regular daily/weekly/monthly benefits (wages, salaries and allowances), compensated absences (paid sick leave, maternity/paternity leave) and other short-term benefits (death grant, education grant, reimbursement of taxes and home leave travel) provided to current employees on the basis of services rendered. All such benefits that are accrued but not paid at the reporting date are recognized as current liabilities within the statement of financial position.

Post-employment benefits

65. Post-employment benefits comprise after-service health insurance, end-of-service repatriation benefits and a pension through the United Nations Joint Staff Pension Fund.

Defined-benefit plans

66. The following benefits are accounted for as defined-benefit plans: after-service health insurance, repatriation benefits (post-employment benefits) and accumulated annual leave that is commuted to cash upon separation from the Organization (other long-term benefits). Defined-benefit plans are those where the Organization's obligation is to provide agreed benefits and therefore the Organization bears the actuarial risks. The liability for defined-benefit plans is measured at the present value of the defined-benefit obligation. Changes in the liability for defined-benefit plans, excluding actuarial gains and losses, are recognized in the statement of financial performance in the period in which they occur. The Organization has chosen to recognize changes in the liability for defined-benefit plans from actuarial gains and losses directly through the statement of changes in net assets. [Add the Organization position as at the reporting date in terms of holding any plan assets as defined by IPSAS 25].

67. The defined-benefit obligations are calculated by independent actuaries using the projected unit credit method. The present value of the defined-benefit obligation is determined by discounting the estimated future cash outflows using the interest rates of high-quality corporate bonds with maturity dates approximating those of the individual plans.

68. After-service health insurance. Worldwide coverage for medical expenses of eligible former staff members and their dependants is provided through after-service health insurance. Upon end of service, staff members and their dependants may elect to participate in a defined-benefit health insurance plan of the United Nations, provided that they have met certain eligibility requirements, including 10 years of participation in a United Nations health plan for those who were recruited after 1 July 2007 and five years for those recruited before that date. The after-service health insurance liability represents the present value of the share of the Organization's medical insurance costs for retirees and the post-retirement benefit accrued to date by active staff. A factor in the after-service health insurance valuation is to consider contributions from all plan participants in determining the Organization's residual liability. Contributions from retirees are deducted from the gross liability together with a portion of the contributions from active staff to arrive at the Organization's residual liability in accordance with cost-sharing ratios authorized by the General Assembly.

69. Repatriation benefits. Upon end of service, staff who meet certain eligibility requirements, including residency outside their country of nationality at the time of separation, are entitled to a repatriation grant, which is based upon length of service, and travel and removal expenses. A liability is recognized from when the staff member joins the Organization and is measured as the present value of the estimated liability for settling these entitlements.

70. Annual leave. The liabilities for annual leave represent unused accumulated leave days that are projected to be settled via a monetary payment to employees upon their separation from the Organization. The United Nations recognizes as a liability the actuarial value of the total accumulated unused leave days of all staff members, up to a maximum of 60 days (18 days for temporary staff) as at the date of the statement of financial position. The methodology applies a last-in-first-out assumption in the determination of the annual leave liabilities, whereby staff members access current period leave entitlements before they access accumulated annual leave balances relating to prior periods. Effectively, the accumulated annual leave benefit is accessed more than 12 months after the end of the reporting period in which the benefit arose and, overall, there is an increase in the level of accumulated annual leave days, pointing to the commutation of accumulated annual leave to a cash settlement at end of service as the true liability of the Organization. The accumulated annual leave benefit reflecting the outflow of economic resources from the Organization at end of service is therefore classified under the category of other long-term benefits, while noting that the portion of the accumulated annual leave benefit that is expected to be settled via monetary payment within 12 months after the reporting date is classified as a current liability. In line with IPSAS 25, Employee benefits, other long-term benefits must be valued similarly to post-employment benefits; therefore, the United Nations values its accumulated annual leave benefit liability as a defined, post-employment benefit that is actuarially valued.

Pension plan: United Nations Joint Staff Pension Fund

71. The Organization is a member organization participating in the United Nations Joint Staff Pension Fund, which was established by the General Assembly to provide retirement, death, disability and related benefits to employees. The Pension Fund is a funded, multi-employer defined-benefit plan. As specified in article 3 (b) of the regulations of the Pension Fund, membership of the Fund shall be open to the specialized agencies and to any other international, intergovernmental organization that participates in the common system of salaries, allowances and other conditions of service of the United Nations and the specialized agencies. The plan exposes participating organizations to actuarial risks associated with the current and former employees of other organizations participating in the Fund, with the result that there is no consistent and reliable basis for allocating the obligation, plan assets and costs to participating organizations. The Organization, along with other participating organizations, is not in a position to identify its share of the defined-benefit obligation, the plan assets and the costs associated with the plan with sufficient reliability for accounting purposes. Therefore, the Organization has treated this plan as if it were a defined-contribution plan in line with the requirements of IPSAS 25. The Organization's contributions to the Fund during the financial year are recognized as employee benefit expenses in the statement of financial performance.

Termination benefits

72. Termination benefits are recognized as an expense only when the Organization is demonstrably committed, without realistic possibility of withdrawal, to a formal detailed plan to either terminate the employment of a staff member before the normal retirement date or provide termination benefits as a result of an offer made in order to encourage voluntary redundancy. Termination benefits to be settled within 12 months are reported at the amount expected to be paid. Where termination benefits fall due more than 12 months after the reporting date, they are discounted if the impact of discounting is material.

Other long-term employee benefits

73. Other long-term employee benefit obligations are benefits, or portions of benefits, that are not due to be settled within 12 months after the end of the year in which employees provide the related service. Accumulated annual leave is an example of long-term employee benefits.

74. Appendix D benefits. Appendix D to the Staff Rules of the United Nations governs compensation in the event of death, injury or illness attributable to the performance of official duties on behalf of the United Nations. Actuaries value these liabilities, and changes in the liability are recognized in the statement of financial performance.

Provisions

75. Provisions are liabilities recognized for future expenditure of uncertain amount or timing. A provision is recognized if, as a result of a past event, the Organization has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. The amount of the provision is the best estimate of the expenditures expected to be required to settle the present obligation at the reporting date. Where the effect of the time value of money is material, the provision is the present value of the amount required to settle the obligation.

76. Uncommitted balances of the appropriations at the end of the budget period and expired balances of appropriations retained from prior periods are to be reported as provisions for credits to Member States. These provisions will remain until the General Assembly decides the manner of their disposal.

Contingent liabilities

77. Any possible obligations that arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Organization are disclosed as contingent liabilities. Contingent liabilities are also disclosed where present obligations that arise from past events cannot be recognized because it is not probable that an outflow of resources embodying economic benefits or service potential will be required to settle the obligations, or the amount of the obligations cannot be reliably measured.

78. Provisions and contingent liabilities are assessed continually to determine whether an outflow of resources embodying economic benefits or service potential has become more or less probable. If it becomes more probable that such an outflow will be required, a provision is recognized in the financial statements of the year in which the change of probability occurs. Similarly, where it becomes less probable that such an outflow will be required, a contingent liability is disclosed in the notes to the financial statements.

Contingent assets

79. Contingent assets are possible assets that arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the effective control of the Organization. Contingent assets are disclosed in the notes when it is more likely than not that economic benefits will flow to the Organization.

Commitments

80. Commitments are future expenses to be incurred by the Organization with respect to open contracts for which the Organization has minimal, if any, discretion to avoid in the ordinary course of operations. Commitments include capital commitments (the amount of contracts for capital expenses that are not paid or accrued by the reporting date), contracts for the supply of goods and services that are not delivered as at end of the reporting period, non-cancellable minimum lease payments and other non-cancellable commitments.

Non-exchange revenue

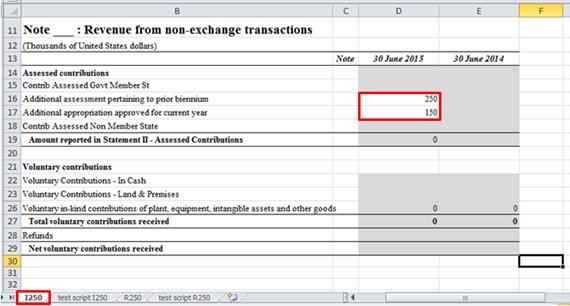

Assessed contributions

81. Appropriations are financed by contributions from Member States that are assessed according to the scale of assessments determined by the General Assembly. These assessments are subject to adjustments in respect of, among other things, supplementary appropriations for which contributions have not previously been assessed, revenue attributable to Member States, contributions resulting from the assessment of new Member States, any uncommitted balance of the appropriations at the end of the budget period and expired balances of the appropriations retained from prior periods that are due to be surrendered to Member States, and credits in the Tax Equalization Fund not required to meet charges for tax reimbursements. Appropriations for the regular budget are approved and assessed for a two-year budget period; the relevant portion of assessed contributions is recognized as revenue at the beginning of each year in the biennium.

Voluntary contributions

82. Voluntary contributions and other transfers, which are supported by legally enforceable agreements, are recognized as revenue at the time when the agreement becomes binding, which is the point when the Organization is deemed to acquire control of the asset. Where cash is received subject to specific conditions, however, recognition of revenue is deferred until those conditions have been satisfied.

83. Voluntary pledges and other promised donations are recognized as revenue when the arrangement becomes binding. Unused funds returned to the donors are netted against voluntary contributions.

84. Revenue received under inter-organizational arrangements represents allocations of funding from agencies to enable the Organization to administer projects or other programmes on their behalf.

85. In-kind contributions of goods above the recognition threshold of USD 20,000 (per discrete contribution) are recognized as assets and revenue once it is probable that future economic benefits or service potential will flow to the Organization and the fair value of those assets can be measured reliably. For vehicles, prefabricated buildings, satellite communication systems, generators and network equipment, a lower threshold of USD 5,000 applies. Contributions in kind are initially measured at their fair value at the date of receipt determined by reference to observable market values or by independent appraisals. The Organization has elected not to recognize in-kind contributions of services, but to disclose in-kind contributions of service above the threshold of USD 20,000 per discrete contribution in the notes to the financial statements.

Exchange revenue

86. Exchange transactions are those in which the Organization sells goods or services in exchange for compensation. Revenue comprises the fair value of consideration received or receivable for the sale of goods and services. Revenue is recognized when it can be reliably measured, when the inflow of future economic benefits is probable and when specific criteria have been met, as follows:

(a). Revenue from sales of publications, books and stamps and from sales by the United Nations Gift Centre is recognized when the sale occurs and risks and rewards have been transferred;

(b). Revenue from commissions and fees for technical, procurement, training, administrative and other services rendered to Governments, United Nations entities and other partners is recognized when the service is performed;

(c). Exchange revenue also includes revenue from the rental of premises, the sale of used or surplus property, guided tours and net currency exchange gains.

87. An indirect cost recovery called a 'programme support cost' is charged to trust funds as a percentage of direct costs including commitments and other 'extrabudgetary' activities to ensure that the additional costs of supporting activities financed from extrabudgetary contributions are not borne by assessed funds and/or other core resources of the Secretariat. The programme support cost is eliminated for the purposes of financial statement preparation, as disclosed in Note 5, Segment reporting. The funding for the programme support cost charge agreed upon with the donor is included as part of voluntary contributions.

Investment revenue

88. Investment revenue includes the Organization's share of net cash pool revenue and other interest revenue [Add other source of investment revenue where applicable]. The net cash pool revenue includes any gains and losses on the sale of investments, which are calculated as the difference between the sale proceeds and book value. Transaction costs that are directly attributable to the investment activities are netted against revenue and the net revenue is distributed proportionately to all cash pool participants on the basis of their average daily balances. The cash pool revenue also includes unrealized market gains and losses on securities, which are distributed proportionately to all participants on the basis of year-end balances.

Expenses

89. Expenses are decreases in economic benefits or service potential during the reporting year in the form of outflows or consumption of assets or incurrence of liabilities that result in decreases in net assets and are recognized on an accrual basis when goods are delivered and services are rendered, regardless of the terms of payment.

90. Employee salaries include international, national and general temporary staff salaries, post adjustment and staff assessment. The allowances and benefits include other staff entitlements, such as pension and insurance subsidies and staff assignment, repatriation, hardship and other allowances. Non-employee compensation and allowances consists of living allowances and post-employment benefits for United Nations Volunteers, consultant and contractor fees, ad hoc experts, International Court of Justice judges' allowances and non-military personnel compensation and allowances.

91. Grants and other transfers include outright grants and transfers to implementing agencies, partners and other entities, as well as quick-impact projects. For outright grants, an expense is recognized at the point at which the Organization has a binding obligation to pay.

92. Supplies and consumables relate to the cost of inventory used and expenses for supplies and consumables.

93. Other operating expenses include acquisition of goods and intangible assets under capitalization thresholds, maintenance, utilities, contracted services, training, security services, shared services, rent, insurance, allowance for bad debt and foreign exchange losses. Other expenses relate to contributions in kind, hospitality and official functions, donations and transfers of assets.

94. Programmatic activities, distinct from commercial or other arrangements where the United Nations expects to receive equal value for funds transferred, are implemented by the United Nations or executing entities or implementing partners to service a target population that typically includes Governments, non-governmental organizations and United Nations agencies. Transfers to implementing partners are fully expensed when disbursed. Binding agreements to fund executing entities or implementing partners, other than outright grants, not paid out by the end of the reporting period are shown as commitments in the notes to the financial statements.

Joint ventures

95. A joint venture is a contractual arrangement whereby the Organization and one or more parties undertake an economic activity that is subject to joint control and can be classified under IPSAS 8, Interests in joint ventures, using three methods:

(a). Jointly controlled entities, which the Organization recognizes using the equity method;

(b). Jointly controlled operations, which are accounted for by recognizing the liabilities and expenses incurred by the Organization, the assets that it controls and its share of any revenue earned;

(c). Jointly controlled assets, where the Organization recognizes its share of the assets, any liabilities that it has incurred, its share of joint liabilities, its share of expenses incurred by the joint venture and revenue earned from the sale or use of its share of the output from the joint venture.

96. The Organization has also entered into joint-venture arrangements for jointly financed operations that give the Organization significant influence, that is, the power to participate in financial and operating policy decisions but not control or jointly control those activities. Under IPSAS 8, the interests in those activities are accounted for using the equity method.

Multi-partner trust funds

97. Multi-partner trust fund activities are pooled resources from multiple financial partners that are allocated to multiple implementing entities to support specific national, regional or global development priorities.

98. They are assessed to determine the existence of control and whether the Organization is considered to be the principal of the programme or activity. Where control exists and the Organization is exposed to the risks and rewards associated with the multi-partner trust fund activities, such programmes or activities are considered to be the Organization's operations and are therefore reported in full in the financial statements.

99. Where joint control exists but the Organization is not considered to be the principal, the activities are considered jointly controlled operations and accounted for as described above.

Changes in accounting policy

[Add relevant notes to changes in accounting policy]

4.4 Note 4: Prior-period adjustments

100. For the following material prior-period adjustments, where there is an impact relating to 20X1, the 20X1 comparative figures at the individual line item were restated.