The September issue of the World Economic Situation and Prospects (WESP) Monthly Briefing from UN DESA’s Development Policy and Analysis Division (DPAD) has just been released. It examines the reciprocal economic sanctions on both the Russian Federation and the European Union; how setting monetary policy within the US is challenged by the labor market situation, and how Brazil is falling into recession, while India expands faster than expected.

The briefing first studies how the reciprocal economic sanctions weigh on the economies of the Russian Federation and the European Union. They have already taken a serious toll on the Russian economy by worsening business sentiment and capital outflows, while in retaliation the Government of the Russian Federation decided in August to impose reciprocal sanctions, despite the risk of higher inflation, which currently poses a serious macroeconomic threat to the Russian economy.

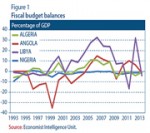

Another topic is the challenges for African oil producers, despite solid oil prices. Even with rich endowment, in particular with a continued solid price level for crude, Africa’s oil producers have seen increasing erosion in their fiscal policy space.

The United States has a new challenge for its monetary policy because of its labor market situation. The good news is that the US economy has continued on the recovery path with an annualized rate of 4.2 per cent from the original estimate of 4.0 per cent. The briefing also notes that Australia alters its environmental policy by abolishing the carbon tax it introduced in 2012, while in Japan the adjustment to the higher consumption tax rate is still unfolding. Western Europe experiences a stalling in growth in the second quarter, with no growth of GDP quarter over quarter.

For the new EU members geopolitical tensions weigh on their economy. The recovery in the region during that period was increasingly driven by domestic demand. As a result, the overall economic sentiment in Central Europe worsened in August. Concerning the economies in transition, import substitution supports industry in the Russian Federation for the Commonwealth of Independent States (CIS) region.

The most severe outbreak of Ebola in history has so far claimed more than 1,000 lives in a number of West African countries. The disease has also had negative economic ramifications, especially in the form of disruptions caused by quarantine measures and additional spending by Governments.

In East Asia, GDP growth in Malaysia and the Philippines strengthens further in the second quarter of 2014, supported by a substantial increase in net exports. Recent data indicate marked differences in growth momentum among East Asian economies. By contrast, GDP growth weakened in other parts of the region, including the high-income economies of Hong Kong Special Administrative Region (SAR) of China, the Republic of Korea and Singapore. In South Asia, India has seen a stronger-than-expected second quarter growth. Growth was boosted by a rebound in investment, a further increase in government consumption and strong exports. The regained optimism about the economy has also lifted India’s stock market.

For the region of Western Asia, the financial costs of the Gaza conflict may reach $8 billion. In addition to the economic consequences, the human toll has been particularly severe in Gaza, with 485,000 people displaced. In Yemen, a reform to lift oil subsidies was approved as part of the plan to address the state budget deficit. Nevertheless, such a reform will need to be complemented by other sound economic and administrative reforms, in order to help the country to avoid continuous dependence on foreign aid and to implement the public investment program.

For Latin America and the Caribbean, Brazil’s economy falls into a technical recession in the first half of 2014. A sharp fall in investment demand is one of the key features of the current economic situation. During the second quarter of 2014, gross fixed capital formation shrank by 5.3 per cent quarter-on-quarter and 11.2 per cent year-on-year. Despite the almost complete political support of the tax reform in Chile, there are concerns among some experts regarding the real effect that the tax reform will have on fiscal revenues and the potential negative impacts on investment, especially for small and medium-sized enterprises.