|

Seventy-sixth session |

|

|

|

Agenda item 140 of the preliminary list* |

|

|

|

Proposed programme budget for 2022 |

|

|

Internal oversight: proposed programme budget for 2022

Report of the Independent Audit Advisory Committee

|

Summary |

|

The present report reflects the comments, advice and recommendations of the Independent Audit Advisory Committee on the proposed programme budget for 2022 of the Office of Internal Oversight Services (OIOS). The Committee continues to be mindful that, in his reform initiative, the Secretary-General called for, inter alia, strengthened evaluation capacity. The Committee is also aware that an effective oversight regime can foster a strengthened evaluation mechanism. To achieve this, the Committee expects that OIOS will continue to review its business model so that it is responsive to the changing environment, including with regard to performance measurement, and to the impact of emerging risks. As the Organization starts to prepare for the return to physical office locations after the coronavirus disease (COVID-19) pandemic, the Committee believes that OIOS could seize this opportunity to review its operations in order to “build back better”. |

|

|

* A/76/50.

I. Introduction

1. The Independent Audit Advisory Committee has undertaken a review of the proposed programme budget for 2022 of the Office of Internal Oversight Services (OIOS) in accordance with paragraphs 2 (c) and (d) of its terms of reference (see General Assembly resolution 61/275, annex). The Committee’s responsibility in this respect is to review the budget proposal of OIOS, taking into account its workplan, and to make recommendations to the Assembly through the Advisory Committee on Administrative and Budgetary Questions. The present report contains the Committee’s comments, advice and recommendations relating to the proposed programme budget for 2022 of OIOS for consideration by the Advisory Committee and the Assembly.

2. The Programme Planning and Budget Division of the Department of Management Strategy, Policy and Compliance provided the Committee with section 30, Internal oversight, of the proposed programme budget for 2022 (A/76/6 (Sect. 30)), as well as relevant supplementary information. OIOS provided supplementary information relating to its budget proposal, which the Committee took into consideration. At its fifty-fourth session, which was held virtually from 21 to 23 April 2021, the Committee allocated a significant proportion of its agenda to discussions with OIOS and the Controller on the proposed budget for OIOS.

3. The Committee would like to acknowledge the efforts of the Programme Planning and Budget Division in expediting the preparation of the internal oversight section of the budget for review by the Committee. The Committee also appreciates the cooperation on the part of OIOS in providing information for the preparation of the present report.

II. Review of the proposed programme budget for 2022 of the Office of Internal Oversight Services

4. The projected resources for OIOS for 2022 from the regular budget (before recosting), combined with other assessed and extrabudgetary resources, totalled $66,381,400, compared with $65,701,900 for 2021, which is an increase of 1 per cent. The increases were in the regular budget and other assessed budget resources, whereas the extrabudgetary resources decreased by 1.1 per cent. The post resources increased by 21 posts, from 282 to 303, as a result of the proposed addition of two posts in the regular budget and the proposed conversion of 19 other assessed budget general temporary assistant positions to posts resources (see table 1).

Table 1

Overall financial and post resources for the Office of Internal Oversight Services, by programme (before recosting)

(Thousands of United States dollars)

Note: Budget figures were based on section 30, Internal oversight, of the proposed programme budget for 2022 (A/76/6 (Sect. 30)) and the relevant supplementary information.

5. Table 2 shows the regular budget resources proposal for OIOS for 2022, compared with the appropriation for 2021. The proposed programme budget for 2022 of OIOS (regular budget) is estimated at $20,989,700 (before recosting), which is a nominal increase of $199,900, or 1.0 per cent, compared with the appropriation of $20,789,800 for 2021. The post resources also increased by two posts, from 114 to 116. The Committee was informed that the increase in the regular budget pertained to two additional posts proposed for the Inspection and Evaluation Division.

Regular budget financial and post resources, by programme (before recosting)

(Thousands of United States dollars)

|

Regular budget |

Financial resources |

|

Post resources |

||||||||

|

2021 appropriation |

2022 estimate |

|

Variance |

2021 appropriation |

2022 estimate |

|

Variance |

||||

|

Amount |

Percentage |

Number of posts |

Percentage |

||||||||

|

|

|

|

|

|

|

|

|

|

|||

|

A. Executive direction and management |

1 485.4 |

1 485.4 |

– |

0.0 |

8 |

8 |

– |

0.0 |

|||

|

B. Programme of work |

17 944.7 |

18 180.0 |

235.3 |

1.3 |

99 |

101 |

2 |

2.0 |

|||

|

Subprogramme 1. Internal audit |

8 341.7 |

8 349.4 |

7.7 |

0.1 |

44 |

44 |

– |

0.0 |

|||

|

Subprogramme 2. Inspection and evaluation |

3 704.7 |

3 945.8 |

241.1 |

6.5 |

22 |

24 |

2 |

9.1 |

|||

|

Subprogramme 3. Investigations |

5 898.3 |

5 884.8 |

(13.5) |

(0.2) |

33 |

33 |

– |

0.0 |

|||

|

C. Programme support |

1 359.7 |

1 324.3 |

(35.4) |

(2.6) |

7 |

7 |

– |

0.0 |

|||

|

Total |

20 789.8 |

20 989.7 |

199.9 |

1.0 |

114 |

116 |

2 |

1.8 |

|||

Note: Budget figures were based on section 30, Internal oversight, of the proposed programme budget for 2022 (A/76/6 (Sect. 30)) and the relevant supplementary information.

6. OIOS further informed the Committee that the main priorities for the 2022 budget included the following: (a) implementation of the Sustainable Development Goals; (b) response to the coronavirus disease (COVID-19) pandemic and lessons learned on United Nations System coherence and business continuity; (c) implementation of the Secretary-General’s reforms of the management, peace and security, and development pillars; (d) strengthening of organizational culture on the basis of respect, equality and results; and (e) implementation of the Secretary-General’s strategies on data, gender parity and environmental sustainability.

A. Executive direction and management

7. As indicated in table 2, the financial and post resources for executive direction and management for 2022 are expected to remain at the same level as those approved for 2021 ($1,485,400).

B. Programme of work

Subprogramme 1

Internal audit

8. The proposed regular budget financial resources for 2022 for subprogramme 1, Internal audit, are expected to increase marginally, from $8,341,700 appropriated in 2021 to $8,349,400 proposed in 2022, but the post resource level will remain at 44 posts (see table 2). The Committee was informed that the nominal increase was attributed, inter alia, to increased requirements for consultancy services to supplement in-house capacity and expertise for the internal audit of the Organization’s infrastructure, cybersecurity, information and communications technology (ICT) security mechanisms and data analytics, as well as contractual services to conduct an external quality assessment of the Internal Audit Division. According to management, the increase was partially offset by reduced requirements for supplies and materials, furniture and equipment, and travel of staff to take into account expenditure patterns and the experience gained in 2020 through increased use of videoconferencing and teleconferencing, whenever possible.

Risk-based workplan process

9. The Committee held discussions with OIOS on the risk-based work planning process and to ascertain how the Internal Audit Division takes organizational risk into account in determining the level of resources required to deliver the programme of work. In line with the position expressed in its previous reports on the budget for OIOS, the Committee continues to believe that using risk assessments to prioritize and allocate audit resources is a best practice. In that regard, OIOS informed the Committee that, for the proposed programme budget for 2022, the Division had continued to employ a refined methodology in assessing its resource requirements, whereby high-risk areas are to be covered in a three-year period, including high-risk cross-cutting areas, whereas medium-risk areas are covered in a five-year period. According to OIOS, lower-risk entities or areas not covered during the preceding period are deemed medium-risk, hence subjected to audit. OIOS further noted that high risks associated with ICT continued to be considered separately and would be covered over a five-year period, instead of a three-year period.

10. The Committee enquired from OIOS the reason for ICT, as a high-risk area, to be subject to a five-year cycle like the medium- to low-risk areas. In response, OIOS informed the Committee that risks associated with ICT were treated separately because the nature of the risks was different and the ICT systems, platforms and applications were used by multiple entities across the system, irrespective of the funding source. OIOS further stated that a five-year cycle instead of a three-year cycle for ICT assignments was used because some of the major ICT change projects required significant resources and their implementation might take multiple years, and because, within the five-year cycle, OIOS prioritized systems (such as data protection) and applications that had the most immediate impact on the reliability, security and transparency of the Organization’s operations.

11. The Committee believes that risks associated with ICT are so critical that considering this item every five years instead of every three years is not an optimum way to address this important focus area. The Committee calls upon OIOS to reconsider this matter as a priority.

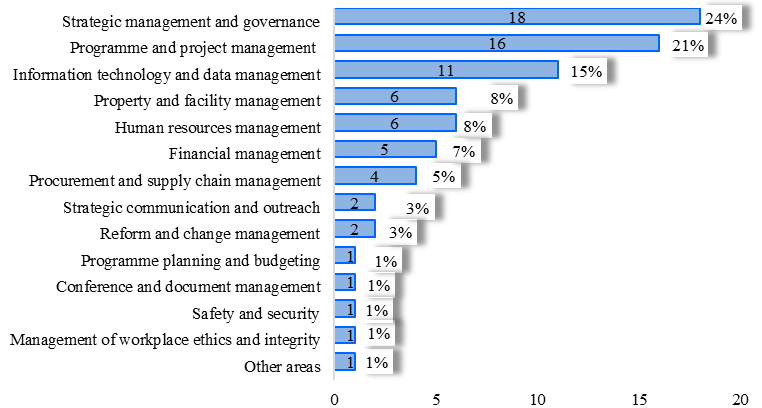

12. OIOS further indicated that, as part of the refinements to the methodology for preparing its risk-based workplans, it continued to adjust the categories of risk used when conducting the entity risk assessments and capacity gap analyses to ensure better alignment with the enterprise risk management framework of the Secretariat. As shown in figure I, the Internal Audit Division plans to undertake 75 assignments in 14 focus areas in 2022. These focus areas mirror the critical risks identified in the Organization’s revised enterprise risk register. The majority (45 assignments) of the proposed assignments for 2022 will focus on three areas: (a) strategic management and governance; (b) programme and project management; and (c) information technology and data management.

Figure I

Assignments of the Internal Audit Division in 2022, by focus area

|

13. The Committee was informed that, in the context of the prevailing situation, including the challenges brought about by the COVID-19 pandemic, OIOS continued to take some efficiency measures, as referred to in paragraph 8. With respect to prioritization, the Committee was also informed that OIOS was planning to use the efficiency gains to fund the proposed external quality assessment of the Internal Audit Division in 2022.

14. The Committee encourages the Internal Audit Division to continue to prioritize its work and focus on aligning its workplan with the organizational risks, including those pertaining to the COVID-19 pandemic, cybersecurity and other emerging risks.

Capacity gap analysis of the Internal Audit Division

15. Within the context of its methodology for work planning, OIOS informed the Committee of the planning assumptions laid out in paragraph 9. According to OIOS, the capacity gap in the Internal Audit Division represents the resources needed to cover risks that cannot be covered within the current resource levels. For the regular budget-funded activities (excluding ICT), OIOS does not foresee a significant capacity gap. According to OIOS, the capacity gap of the Internal Audit Division for 2022 has become more apparent in extrabudgetary funded activities (2.4 staffing gap) and in ICT, which covers the entire ICT audit universe, regardless of funding, with a 3.2 staffing gap. Despite this shortfall, OIOS informed the Committee that no additional resources had been requested for 2022 and that OIOS would continue to adjust the methodology used to assess ICT risks and identify gaps in capacity that would inform its future resource requests.

16. The Committee remains cognizant of the prevailing environment that the Organization is facing and of the budget guidance provided. The Committee is also aware that, through prioritization and efficiency gain measures, the Internal Audit Division has been able to address the critical risks of the Organization without needing additional resources, especially in the regular budget component of its work. On that note, the Committee endorses the resource requirements submitted for the Division.

Subprogramme 2

Inspection and evaluation

17. As shown in table 2, the proposed regular budget financial resources for 2022 for subprogramme 2, Inspection and evaluation, amount to $3,945,800, representing an increase of $241,000, or 6.5 per cent, compared with the appropriation for 2021, which stood at $3,704,700. The post resources also increased from 22 posts approved in 2021 to 24 posts proposed in 2022. According to management, the increase in the proposed budget resources is due to the proposed establishment of two new posts, a Deputy Director (D-1) and an Evaluation Officer (P-4), to provide support for strengthening the evaluation function within the Secretariat and for delivering OIOS evaluations in an efficient and effective manner. The increase is partly offset by reduced requirements for travel of staff to take into account the experience gained in 2020 through increased use of videoconferencing and teleconferencing, whenever possible.

Risk assessment and workplan process

18. As noted in its previous report (A/75/87), OIOS changed the way that the Inspection and Evaluation Division was addressing the evaluation needs of the Organization, in that some departments, such as the Department of Management Strategy, Policy and Compliance and the Department of Operational Support, would be subject to performance auditing by the Internal Audit Division rather than through programme evaluations conducted by the Inspection and Evaluation Division, and that the evaluation of the remaining entities would be conducted at the subprogramme level rather than at the programme level (in other words, rather than at a high level). Under the new subprogramme-focused approach, OIOS indicated that it would continue to assess and rank subprogrammes taking into consideration the Secretariat’s enterprise risk management risk register information, as well as risks emanating from United Nations reform initiatives and support for the Sustainable Development Goals. OIOS further noted that, in the conduct of its evaluations, the Inspection and Evaluation Division would integrate the strategies of the Secretary-General on data, gender parity and environmental sustainability, as well as considerations of the impact of COVID-19 on programme performance for mandate implementation.

Positions to support a strengthened evaluation capacity

19. Accordingly, in the context of providing support for the reform initiative of the Secretary-General, in which he called for a strengthened evaluation capacity, the Committee was informed that the current proposal included the establishment of a dedicated capacity within the Inspection and Evaluation Division to strengthen the Secretariat’s self-evaluation function and to deliver innovative new evaluation support and synthesis products.

20. The Committee enquired from OIOS how the two posts would support the self-evaluation capacity of the Secretariat and why those posts were not requested by management instead of OIOS. In response, the Committee was informed that the D-1 post incumbent would be expected to act as a deputy to the Director of the Inspection and Evaluation Division, supporting in the overall management of the Division, and would lead OIOS efforts in providing independent evaluation support to the Organization, as mandated in the OIOS founding resolution (General Assembly resolution 48/218 B) and in the Regulations and Rules Governing Programme Planning, the Programme Aspects of the Budget, the Monitoring of Implementation and the Methods of Evaluation. Under the Regulations and Rules, OIOS is mandated to perform the functions of a “central evaluation unit” by, inter alia, providing methodological support to entities in the conduct of their own evaluations; acting as a source of evaluation expertise for the Organization; providing and ensuring quality standards for the conduct of evaluations by entities; providing ad hoc advice on the conduct of evaluations; developing and disseminating evaluation tools and guidelines; and ensuring the overall coordination of evaluation planning across the Secretariat. OIOS further contended that, in requesting those two positions, OIOS was fulfilling its responsibilities as the central evaluation unit and that the Business Transformation and Accountability Division of the Department of Management Strategy, Policy and Compliance had resources to fulfil its own responsibilities to support self-evaluations by the Secretariat.

21. The Committee recalls its previous observation in paragraphs 18 to 22 of its report A/68/86 with regard to OIOS deciding to eliminate the post at the D-1 level (Deputy Director) in the Inspection and Evaluation Division, a decision that the Committee did not endorse in the light of the capacity gap in the Division at the time. For several years, the Committee has put on record its support for an increase in resources available to the Inspection and Evaluation Division of OIOS, and it continues to maintain that position.

Capacity gap analysis of the Inspection and Evaluation Division

22. With regard to the capacity gap analysis, the Committee was informed that the initial capacity assessment and gap analysis of the Inspection and Evaluation Division had been made within the revised context, which envisaged 162 subprogrammes, up from 142 reported in 2020. According to OIOS, the following assumptions informed the Division’s capacity gap analysis: (a) the analysis would not include the three Development Coordination Office subprogrammes for which funding was provided by that Office; (b) it was expected that 1.33 evaluations would be undertaken per team of two evaluators per year; (c) full evaluation of subprogrammes and special political missions would be undertaken in a period of eight years; and (d) a vacancy rate of 9 per cent (excluding the D-2 Director and General Service staff) would be applied.

23. In order to meet its goal of evaluating every subprogramme once in an eight-year period, OIOS indicated that the Inspection and Evaluation Division would have to evaluate 20 subprogrammes per year, requiring 30 staff annually. According to OIOS, however, the Division has 17 available staff to conduct evaluations, leaving a gross annual capacity gap of 15 staff after applying the 9 per cent vacancy rate on the available staff.

24. To address the gap, OIOS informed the Committee that it planned to do the following: (a) group common subprogrammes into similar thematic clusters to reduce the number of separate subprogramme evaluations required; (b) focus on the 93 subprogrammes assessed as either of very high or high risk on an eight-year cycle; and (c) strengthen entity evaluation capacity within the Secretariat through training, support, guidance and tools for the conduct of high-quality evaluations by entities (for which one post at the D-1 level and one post at the P-4 level have been requested). The aforementioned strategies are expected to reduce the capacity gap to five staff members.

25. The Committee enquired from OIOS what the impact of the capacity gap would be on the work of the Inspection and Evaluation Division and was informed that the gap of five posts would affect the ability of the Division to cover very high or high-risk subprogrammes within an eight-year cycle. That is, without the five staff, the Division would not be able to cover all 93 very high or high-risk subprogrammes over eight years.

26. As noted above, the Committee has consistently supported a stronger and well-staffed Inspection and Evaluation Division. This view is all the more valid in the context of the 2030 Agenda for Sustainable Development and the reform initiative of the Secretary-General, which puts greater emphasis on a robust evaluation capacity. The Committee continues to believe that the Division needs to be strengthened if it is to execute its mandate effectively. The Committee, therefore, supports the proposal to reinstate the post at the D-1 level and create a post at the P-4 level in the Division. The Committee, nevertheless, continues to be concerned that, in the light of the current situation, the Division may not be able to address all areas in a timely manner. The Committee, therefore, encourages OIOS to ensure adequate prioritization so as to focus on the high-risk subprogrammes within the eight-year evaluation cycle.

Subprogramme 3

Investigations

27. The proposed regular budget financial resources for 2022 for subprogramme 3, Investigations, amount to $5,884,800, representing a nominal net decrease of 0.2 per cent compared with the appropriation of $5,898,300 for 2021. The post resources remained the same, at 33 posts (see table 2). According to management, the decrease reflects reduced requirements under consultants, contractual services, general operating expenses, and furniture and equipment. This reduction was partly offset by increased requirements, mainly under travel of staff, to take into account increased travel of investigators to conduct investigations on cases of allegations of sexual harassment and fraud, in particular in offices away from Headquarters, that were either cancelled or postponed owing to the COVID-19 pandemic.

28. During the review, the Committee was informed that the Investigations Division continued to address the issues identified in the Committee’s previous reports, especially the recruitment and retention of staff in the Division. As reported by the Committee in paragraph 38 of its report A/75/783, the vacancy rate in the peacekeeping section of the Division had declined from a high of 25.8 per cent reported as of June 2019 to 6.6 per cent as at 31 December 2020. Upon further follow‑up, the Committee was informed that, while the peacekeeping section vacancy rate had increased, albeit marginally, to 8.2 per cent as at 31 March 2021, the regular budget vacancy rate had increased to 33.3 per cent during the same period.

29. The Committee acknowledges that OIOS has made some progress of late in addressing the vacancy situation. However, the Committee continues to be concerned with the number of vacancies in OIOS and believes that this risk ought to be carefully managed.

Trend analysis and workplan process of the Investigations Division

30. During its deliberations, the Committee was provided with relevant trend analyses of the activities of the Investigations Division. According to OIOS, those analyses had formed the basis for the workplan for 2022. Specifically, the Committee looked at the intake levels for the investigation matters that came to the Investigations Division and was informed that, after exhibiting a sustained upward trend in reported matters since 2015, OIOS projected that the number would remain at 2020 levels until 2022. It is expected that by the end of 2021, the Division will have received 1,240 cases, compared with 1,253 in 2020 (see figure II).

Figure II

Trend analysis of cases received by the Investigations Division

|

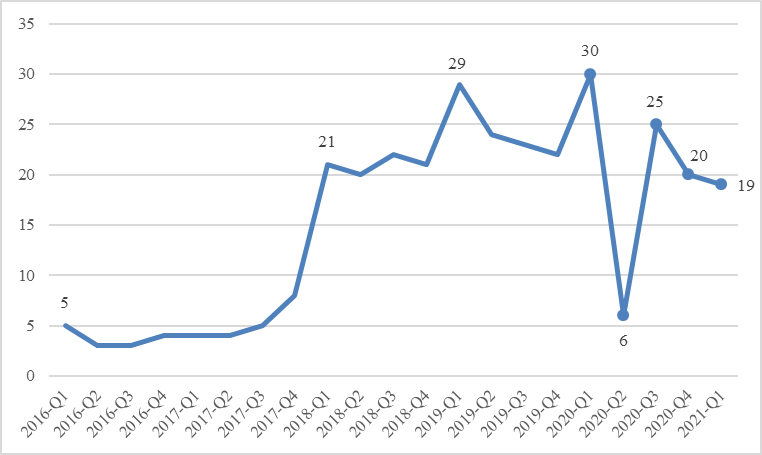

31. With respect to sexual harassment complaints, the Committee was informed that the number had declined from a high of 30 reported in the first quarter of 2019 to 19 in the first quarter of 2021. As shown in figure III, the second quarter of 2020 saw one of the lowest number of cases reported, with six cases, probably reflecting the remote working environment in which the Organization operated.

Figure III

Sexual harassment complaints

|

Abbreviations: Q1, first quarter; Q2, second quarter; Q3, third quarter; Q4, fourth quarter.

Capacity gap analysis of the Investigations Division

32. In determining the capacity gap of the Investigations Division for 2022, OIOS informed the Committee of the planning assumptions used, including: (a) reporting of cases plateaued in 2020 and would remain at that level until 2022; (b) each investigator would handle up to five open investigations and complete six investigations per year; (c) the forecast for open and completed regular budget and extrabudgetary investigations in 2021 would remain at 2020 levels; and (d) the high vacancy rate would be addressed.

33. According to OIOS, the capacity gap of the Investigations Division represents the available capacity versus that which is required to handle the expected caseload within the timeliness targets. The Committee was informed that OIOS was making every effort to fill the positions as soon as possible, and that once the vacancies were addressed, OIOS did not expect a capacity gap to complete the 130 investigations projected for 2022.

34. In view of the above, the Committee endorses the resource requirements of the Investigations Division, which reflect the maintenance of the same resource levels.

C. Programme support

35. The proposed regular budget resources for programme support for 2022 amounts to $1,324,300. The post resources remain at seven posts.

III. Conclusion

36. The members of the Independent Audit Advisory Committee respectfully submit the present report, containing the Committee’s comments and recommendations, for consideration by the General Assembly.

(Signed) Janet St. Laurent

Chairman, Independent Audit Advisory Committee

(Signed) Agus Joko Pramono

Vice-Chair, Independent Audit Advisory Committee

(Signed) Dorothy A. Bradley

Member, Independent Audit Advisory Committee

(Signed) Anton A. Kosyanenko

Member, Independent Audit Advisory Committee

(Signed) Imran Vanker

Member, Independent Audit Advisory Committee