World Economic Situation And Prospects: September 2019 Briefing, No. 130

- Prolonged trade tensions exacerbating the cyclical slowdown in the global economy

- Global automobile production contracts amid higher tariffs and policy uncertainty

- Further easing of macroeconomic policies as external headwinds to growth rise

English: PDF (168 kb)

Global issue: Trade conflict a threat to global growth

Trade tensions between China and the United States re-escalated in August, following the announcement by the United States that it will impose tariffs on a further $300 billion of Chinese imports. In retaliation, China introduced additional tariffs on $75 billion of imports from the United States. These developments triggered sharp movements in global equity markets, a decline in global oil prices and higher capital outflows from the emerging economies. As the trade disputes threaten to become even more pervasive, the global growth outlook has darkened.

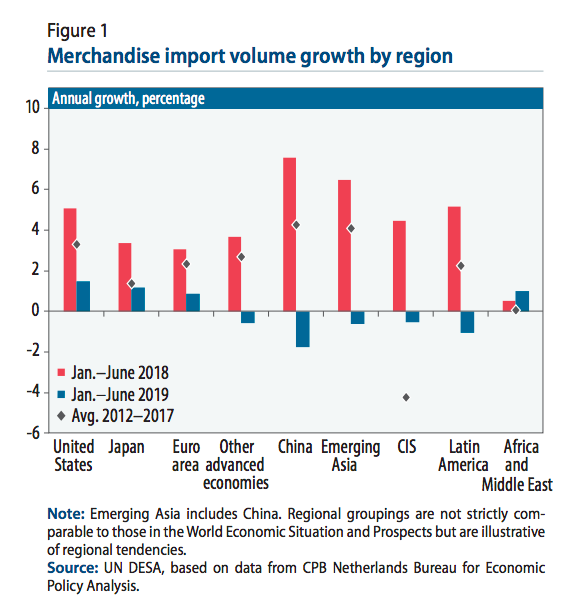

The protracted period of high trade tensions is exacerbating an ongoing cyclical slowdown in global economic activity. In tandem with slowing industrial production, world trade growth has decelerated sharply over the past year. For most developed and developing regions, trade growth has not only weakened compared to 2018, but has also fallen well below the average growth rate between 2012 to 2017 (Figure 1). Alongside recent monetary policy shifts by major central banks, persistent uncertainty surrounding trade actions has induced heightened investor risk aversion and financial market volatility. In many countries, there are signs that the deterioration in business confidence has started to dent investment growth.

The protracted period of high trade tensions is exacerbating an ongoing cyclical slowdown in global economic activity. In tandem with slowing industrial production, world trade growth has decelerated sharply over the past year. For most developed and developing regions, trade growth has not only weakened compared to 2018, but has also fallen well below the average growth rate between 2012 to 2017 (Figure 1). Alongside recent monetary policy shifts by major central banks, persistent uncertainty surrounding trade actions has induced heightened investor risk aversion and financial market volatility. In many countries, there are signs that the deterioration in business confidence has started to dent investment growth.

Given inconclusive trade negotiations, there is a growing risk that trade tensions will further intensify going forward. If the United States expands trade restrictive measures, for example by imposing blanket tariffs on automobile imports, affected countries will likely respond with retaliatory measures. Such a spiral of further tariffs and retaliations would spread beyond the involved parties, impacting the developing economies through both direct and indirect channels.

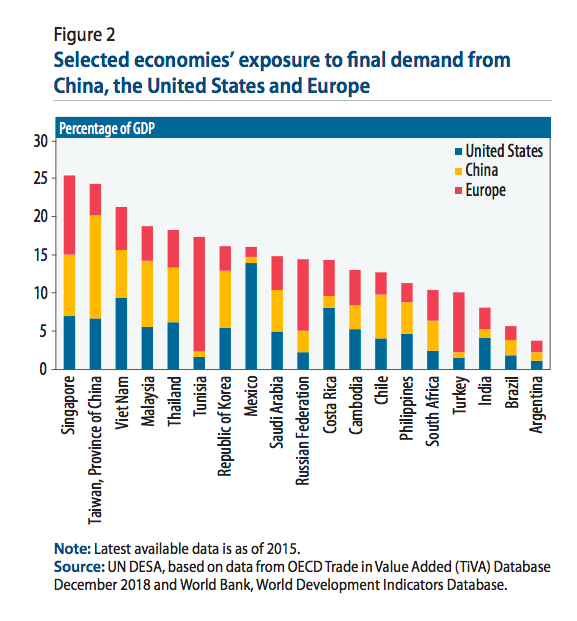

Higher tariffs and prolonged weak sentiments could significantly dampen domestic demand growth in the major economies, namely China, the United States and Europe. This will directly affect economies with a high final demand exposure to these large markets. Figure 2 shows that China is the main source of final demand for many East Asian exporters today, including Malaysia, the Republic of Korea, and Thailand. For these economies, this reflects a marked change in the trade structure compared to a decade ago, when a larger share of exports was catered towards demand in the United States and Europe. In contrast, countries such as Costa Rica and Mexico remain much more vulnerable to a growth slowdown in the United States, while the Russian Federation and Turkey are more sensitive to changes in European demand. In addition, slower growth in China and the United States would also weigh on global demand for commodities, adversely impacting commodity-dependent countries, including in Africa and Latin America.

A worsening of trade tensions will also have an indirect effect on third countries through disruptions to global value chains (GVCs). Countries that are deeply integrated into GVCs would be the most affected by a decrease in demand for intermediate inputs, as the imposition of tariffs not only hurts assembling countries, but also suppliers along production chains. Notably, the trade disputes have amplified cyclical headwinds in the electronics and automobile sectors, both of which have extensive cross-country production networks. In the first half of 2019, world semiconductor billings declined by almost 15 per cent compared to the same period last year. Meanwhile, global automobile sales have contracted in the first seven months of the year, as discussed later.

Furthermore, an intensification of the trade conflict would fuel greater uncertainty in the global environment, leading to an increased likelihood of firms postponing or cancelling investment plans. Coupled with softening global demand and country-specific issues, recent data reveals that investment growth has slowed sharply in many developing economies, including Mexico, the Republic of Korea, South Africa and Singapore.

Several developing countries, however, stand to benefit in the short term from a diversion in trade flows, as firms seek to source inputs from countries that are not directly affected by the tariffs. There are also indications that manufacturers are looking to relocate production from China to other countries, particularly those in the East Asian region. Nevertheless, reconfigurations to existing GVCs are likely to proceed very gradually, given the complexity of production processes and uncertainty over the future policy landscape. Firms would also need to assess a host of other factors when choosing a new production location, such as the quality of infrastructure, labour force skills, and domestic regulation.

Several developing countries, however, stand to benefit in the short term from a diversion in trade flows, as firms seek to source inputs from countries that are not directly affected by the tariffs. There are also indications that manufacturers are looking to relocate production from China to other countries, particularly those in the East Asian region. Nevertheless, reconfigurations to existing GVCs are likely to proceed very gradually, given the complexity of production processes and uncertainty over the future policy landscape. Firms would also need to assess a host of other factors when choosing a new production location, such as the quality of infrastructure, labour force skills, and domestic regulation.

Moreover, while trade disputes between China and the United States may create opportunities for a few countries, the overall effects on the global economy are negative. Not only would current unresolved trade tensions prolong the weakness in global trade and demand, but they risk triggering a wider spread of protectionist measures by other countries, derailing global economic activity. Importantly, the prolonged trade conflict could inflict long-lasting damage on global development prospects. A slowdown in investment would result in weaker job creation while constraining productivity growth. In many developing countries, disruptions to GVCs could also considerably undermine growth, given the important role that GVC-related trade has played in raising income per capita and productivity. The loss of income could impact social spending, whereas for households, the increase in prices of goods as a result of tariffs lowers purchasing power and consumer welfare, particularly if domestic and imported goods are not easily substitutable.

Amid constrained macroeconomic policy space, an escalation of trade protectionism in the world economy poses a major risk to global growth and the realization of the 2030 Agenda. The inaugural SDG Summit, which will be held later this month, presents a valuable opportunity for world leaders to engage in productive dialogue and discuss strategies to address the current global economic challenges, including a strengthening of the rules-based multilateral trading system.

Developed economies

North America and Europe: Automobile production contracts amid slowdown in trade

Following a 3.4 per cent contraction in 2018, production of automobiles in the United States declined by a further 2 per cent in the first seven months of 2019. In the European Union, manufacture of motor vehicles declined by over 10 per cent in the first half of 2019. This weak performance of the automobile sector forms part of a broad global trend. In 2018, world production of passenger cars declined by 0.9 per cent, marking the first global contraction in this sector since the global financial crisis in 2008-09. Available data point to an even sharper contraction in 2019. The automotive industry is one of the world’s largest economic sectors and is labour and capital intensive. Its dynamics have an important impact on global growth, employment and overall development.

Weak global production is widely attributed to falling demand in China, where automobile sales between January–July 2019 were 11.4 per cent lower compared to last year. Passenger car registrations have also declined significantly in Australia, Canada, India, the United States and Europe. Germany is the world’s biggest automotive exporter, and Europe is particularly sensitive to falling global demand for automobiles.

Global trade tensions have significantly disrupted production in the automobile sector, both through the direct impact of higher tariffs and the indirect impact of policy uncertainty. As highlighted earlier, the automobile sector is deeply embedded in global and regional value chains, with complex and geographically dispersed production networks, and is therefore highly sensitive to disruptions in trade. The imposition of steel tariffs in the United States in March 2018 has been felt acutely by the automotive networks connected to North America; while an extended period of uncertainty during the negotiations surrounding the US-Canada-Mexico Agreement also disrupted North American automotive production networks. In April 2018, China and the United States raised tariffs on bilateral imports of many vehicles and vehicle parts, although China subsequently suspended certain tariffs in response to disruptions to the sector. The United States Government has postponed until November 2019 a decision on threatened tariffs of up to a 25 per cent on all imports of cars and car parts, prolonging the policy uncertainty facing the sector.

In addition to trade tariffs, the global automobile sector is undergoing a transition related to environmental standards. For example, tighter emissions standards in Europe have led to some temporary disruption of production networks, while the New Energy Vehicle incentives in China have impacted demand for traditional internal combustion engine vehicles. At the same time, car sharing and ride sharing schemes are becoming more popular, depressing demand for ownership. These pressures can be expected to continue to impact automobile demand patterns going forward.

Developed Asia: Japanese exports declined over the first half of 2019

Over the first half of 2019, Japan’s export volumes declined by 5.6 per cent compared to the same period last year. Import volumes also fell, but to a smaller extent, by 1 per cent. Given the rapid decline in exports, Japan’s trade balance remains in deficit. The recent decline in exports reflects some shift in trade patterns. Exports to other Asian countries, including China and the Republic of Korea, have contracted, with a sharp contraction in exports of steel, semiconductor parts and semiconductor-making equipment. In contrast, exports of automobiles and semiconductor-making equipment to the United States have increased. While Japan’s overall imports of energy and metal products contracted, its imports of these products from the United States expanded rapidly.

Economies in transition

CIS: China is an important export destination for the region

Economic and political agreements concluded by the countries in the Commonwealth of Independent States (CIS) have led to a certain fragmentation of regional trade patterns. On the one hand, the Eurasian Economic Union (EAEU) of Armenia, Belarus, Kazakhstan, Kyrgyzstan and the Russian Federation, established in 2015, registered a steady increase in its internal trade in 2017–2018. On the other hand, Georgia (not a member of the CIS), Republic of Moldova and Ukraine in 2014 signed Association Agreements with the EU, containing Deep and Comprehensive Free Trade Agreements. Concurrently, the EU became the major export destination for those countries, absorbing 65.7 per cent of exports of the Republic of Moldova in 2017 and 42.7 per cent of Ukrainian exports in 2018. The EAEU has also concluded other agreements, including a free-trade agreement with Viet Nam; while Georgia has reached a free trade agreement with China, which entered into force in 2018. Mutual trade restrictions between the Russian Federation and most of the OECD countries, adopted after the Crimea conflict, as well as trade restrictions between the Russian Federation and Ukraine, are constraining the region’s trade growth potential.

The direct impact of the ongoing trade disputes on the region is likely to be limited, given the relatively low degree of participation in global production chains. However, weaker energy prices and slowing global demand, especially from China, could significantly affect the region’s energy exporters. For Kazakhstan and the Russian Federation, China is an important export market. Until the recent decision by the Russian Gazprom to purchase natural gas from Central Asia, China was also the only importer of Turkmenistan’s natural gas. In July, the Russian Federation reached an agreement with China to significantly increase soybean and wheat exports to compensate for reduced imports from the United States, and there are also plans to increase pork exports to China.

Developing economies

Africa: High vulnerability to trade tensions amid deepening intra-regional trade

The United States-China trade tensions have contributed to slowing demand in Africa’s key trading partners, including China and the euro area. This has led to lower commodity prices and weaker demand for Africa’s commodity exports as well as some turbulence in currency markets. In the first week of August, amid a sharp escalation in the trade conflict and increased risk aversion by investors, emerging market currencies softened broadly. South Africa’s rand, in particular, slipped to seven-week lows against the dollar.

African countries could be severely affected by a further escalation of the trade conflict between China and the United States. China is actually Africa’s single largest trading partner, while the United States places fifth. Analysis by the IMF indicates that intensified trade tensions and increased trade policy uncertainty in the United States, slower growth in China, lower commodity prices and tighter financial conditions have the potential to lower growth in sub-Saharan Africa by 2 percentage points this year and 1½ percentage points next year. The economies most affected would be commodity exporters, countries with significant linkages with China and global markets, and those with large refinancing needs.

However, against the backdrop of increased trade barriers externally, the continent has been piecing together the world’s largest free-trade zone internally. In July, the leaders of Benin and Nigeria signed the accord for the African Continental Free Trade Area at a special African Union meeting in Niger’s capital, Niamey. The accord has now been signed by 54 of 55 member states of the African Union.

East Asia: Slowing growth prompts policy easing measures

The protracted trade conflict between China and the United States is visibly affecting East Asia’s export growth. In the second quarter of 2019, exports contracted across most economies in the region, with Indonesia, the Republic of Korea and Singapore experiencing the largest declines. Leading indicators such as new export orders and business sentiments have also continued to deteriorate, pointing towards continued external sector weakness in the coming months. A further escalation of trade tensions poses a significant downside risk to East Asia’s growth, particularly given its potential to severely disrupt global and regional production networks. As the continued expansion of tariff actions continues to fuel global policy uncertainty, the region’s investment prospects have also dimmed.

Given the challenging external environment, policymakers are increasingly undertaking measures to support short-term growth. Over the past few months, several central banks in the region have lowered interest rates, including Indonesia, the Philippines, the Republic of Korea and Thailand. China also recently introduced some reforms to its interest rate policy, aimed at improving the monetary policy effectiveness and lowering financing costs to the real economy. A few countries have also announced plans to adopt more expansionary fiscal policies. In August, Thailand unveiled a fiscal stimulus package of $10 billion (2 per cent of GDP), which include measures to support farmers and to boost the tourism sector.

South Asia: Overlapping trade and political tensions

The global trade disputes overlap with political tensions and unsettled disputes in South Asia. The Islamic Republic of Iran remains in an economic and currency crisis amid global political pressures that have severely impacted the country’s oil exports. Estimates for July suggest that oil exports may have dropped to as low as 100,000 barrels per day, from almost 2.5 million barrels per day exported in April 2018—just before the United States withdrew from the nuclear deal.

Increased tensions between the two largest economies in the region, India and Pakistan, have led to a suspension of bilateral trade. While bilateral trade between the two countries is relatively small (1–2 per cent of total exports) the textile industry in Pakistan relies on imports of chemicals and cotton from India. These materials are difficult to substitute in the short term due to time required for technological adjustments, and the textile sector is likely to suffer some short-term disruption. However, some trade may be re-routed through Dubai. Estimates suggest that indirect trade via Dubai may already be twice as high as the direct bilateral exchange. Import tariffs in the United States also have a small impact on India. Amidst the political and trade tensions, some countries may benefit from shifting trading routes and manufacturing centres, notably Bangladesh. The Asian Development Bank estimates that trade diversion could add around $400 million to merchandise exports from Bangladesh, and raise GDP by 0.2 per cent. Similarly, neighbouring Myanmar may expand labour-intensive manufacturing.

Western Asia: Last year’s steep currency devaluation is impacting Turkey’s trade performance

In June, Turkey’s current account balance registered a 12-month rolling surplus of $538 million. It is rare for Turkey to record a sizeable current account surplus over a full year. One of the drivers of the country’s rapid growth since the early 2000s was substantial foreign capital inflows, which financed growing current account deficits. However, since a sudden stop of foreign capital inflows last year, the Turkish economy has been struggling to adjust to a new set of macroeconomic constraints. While the tightening of domestic demand was expected to reduce imports, the steep devaluation of the Turkish lira was expected to increase exports amid increased price competitiveness. Indeed, Turkey’s import volumes have contracted by an average of 20.3 per cent on a year-on-year basis since August 2018, while export volumes have increased by 10.6 per cent. Over the same period, the export unit value index has contracted by an average of 4.3 per cent while the import unit value index has barely changed. As Turkey’s terms-of-trade have deteriorated since the currency devaluation, the rise in export earnings is modest relative to the sizeable increase in export volumes. Modest but resilient export growth has been seen in the automotive sector, which accounts for 15 per cent in total exports. Meanwhile, import adjustments have been concentrated in the precious metal and consumer durables sectors.

Latin America and the Caribbean: United States-China trade conflict clouds the growth outlook

The United States-China trade conflict is weighing on the economic outlook for Latin America and the Caribbean even as some countries have seen short-term gains from a diversion of trade flows. Among the region’s main beneficiaries are Brazil’s soybean producers and Mexico’s machinery and automotive sectors. After China imposed in July 2018 a 25 per cent tariff on soy imports from the United States, it increasingly turned to Brazil to meet its needs. China’s soybean imports from Brazil rose by 37 per cent in 2018, offsetting a 50 per cent decline in soybean imports from the United States. In the first half of 2019, however, an outbreak of African Swine Fever has led to a sharp drop in China’s overall demand for soy, which is largely used for animal feed. As a result, China’s soybean imports from Brazil have also fallen. Meanwhile, Mexico, has benefited from an increase in exports of vehicles, auto parts, electronics and machinery to the United States. In all of these categories, Mexico’s market share in the United States has edged up since early 2018, whereas China’s fell sharply.

Although certain sectors are gaining from the continuing trade conflict, the overall impact on the region is likely to be negative. There are several channels through which economic activity in Latin America and the Caribbean would be further affected. First, China and the United States combined account for 55 per cent of the region’s exports. Slower demand growth in the two countries would thus have a notable impact on the region. Second, the trade conflict is exerting downward pressure on commodity prices, including oil and metals. In early August, copper prices fell to the lowest level in two years, causing export revenues in Chile and Peru to decline significantly. Third, the trade conflict adds to economic uncertainty, which is already elevated in several countries, including Argentina, Brazil and Mexico, due to domestic policy issues. High levels of uncertainty are adversely affecting capital flows to the region and investment, dampening the prospects for recovery.

Follow Us