World Economic Situation And Prospects: August 2020 Briefing, No. 140

Varying impact of the COVID-19 pandemic on the labour markets of developed countries

Varying impact of the COVID-19 pandemic on the labour markets of developed countries

The outbreak of the COVID-19 pandemic and the resulting severe restrictions on economic and social activities had a profoundly disruptive impact on labour markets in virtually every part of the world, including in the OECD countries—the group mostly characterised by high-income, industrially-advanced and diversified economies, which includes, among others, the United States, CANZ group of countries, most of the European Union (EU) and Japan. The aggregate OECD unemployment rate stood at 5.2 per cent in February 2020, as several OECD member states entered 2020 with historically low unemployment figures, but by April it had increased to 8.5 per cent, its highest value in a decade. The employment crisis disproportionately affected youth, women and workers with a low degree of social protection, including migrant workers.

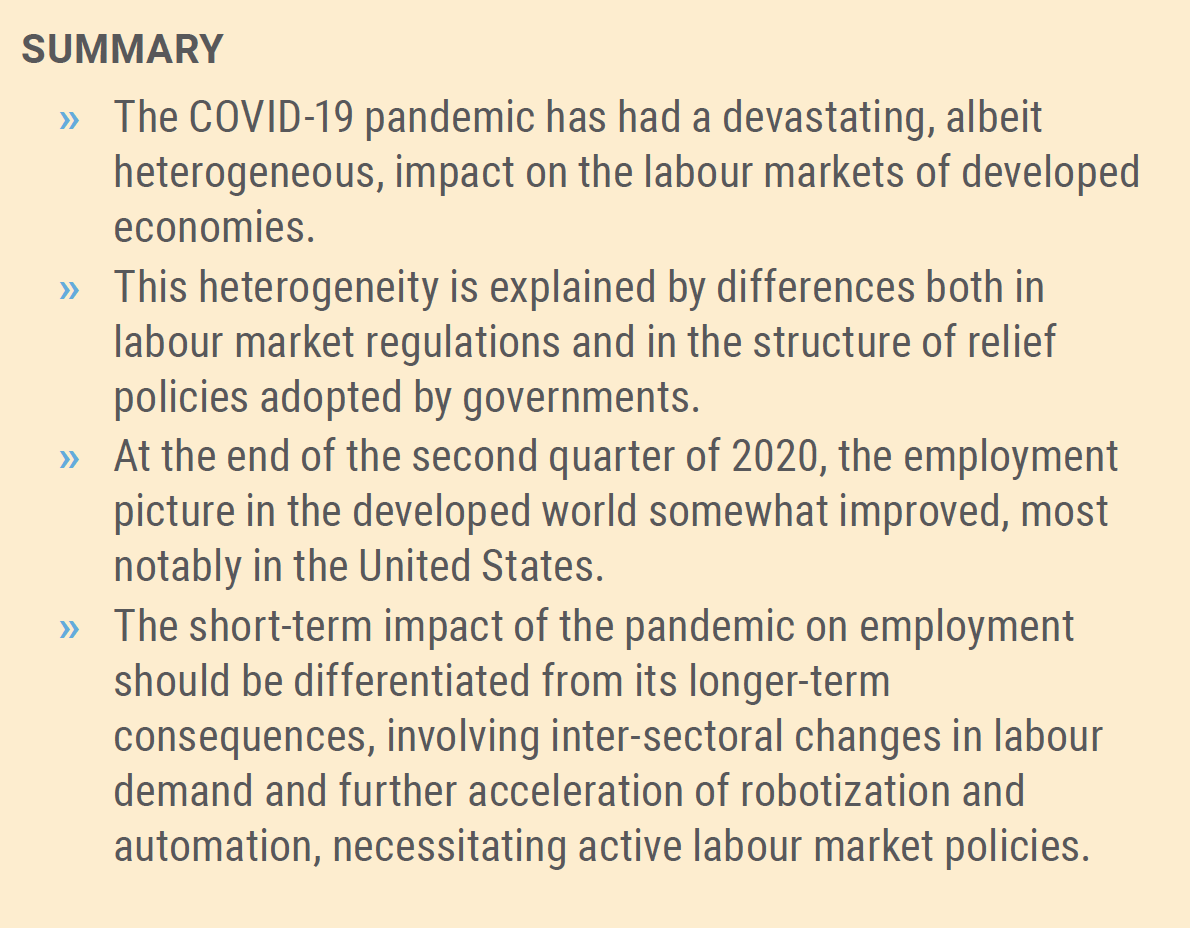

The impact of the pandemic on the labour market conditions in the OECD (at least on headline unemployment numbers) was, however, quite heterogeneous across countries. This heterogeneity can be seen in Figure 1, which shows changes in the OECD countries’ unemployment rates from January to April 2020, when those rates in many countries were pushed to historical highs by supply-chain disruptions, mandatory lockdowns, border closures and shifts in consumer behaviour dampening aggregate demand. The unemployment rate in April 2020 has soared into double-digits in the United States and in Canada, while remaining virtually unchanged in Germany and Japan, despite severe economic setbacks experienced by these countries. Moreover, seemingly paradoxically, in a number of OECD countries the unemployment rate has declined, including in Italy, which introduced one of the most stringent lockdowns and which significantly depends on the tourism industry brought to a standstill by the pandemic. These reductions in the unemployment rate, however, reflect not only the effect of newly introduced domestic policies, but also sharp contractions in the labour force—a precipitous drop in the participation rate, especially among those who were engaged in temporary or seasonal jobs, for example in the tourism sector. Many of these jobs were not shielded from layoffs by the emergency labour regulations introduced in Italy as part of the economic stimulus package.

Different factors are behind the diverging unemployment trends

Different factors are behind the diverging unemployment trends

There are multiple factors explaining such a divergent behaviour of labour markets in the OECD area in response to the pandemic-caused recession, apart from the varying sectoral/industry compositions of those economies. In fact, some economies such as the Czech Republic and Germany that are more open and more exposed to global or regional production chains, showed remarkable stability in their unemployment rates, in contrast to the relatively closed United States economy.

It is important to note that there are pronounced differences with respect to the labour market regulations and the degree of employment protection among those countries, in particular between the United States and most of continental Europe. One of the quantitative indicators of labour market flexibility, the Employment Flexibility Index 2020, ranks the United States at the top, with the index value of 92.4 (on a scale of 0 to 100), while the respective values equal 63.5 for Germany and only 38.4 for France. There are also different approaches in public policies with respect to cyclical fluctuations in labour demand—the United States policy mostly focuses on providing unemployment benefits, while the EU countries actively apply job retention policies to avoid layoffs and to protect institutional memory and accumulated work experience. Concurrently, the countries exhibit different degrees of sensitivity of employment to swings in business cycles, with much lower unemployment volatility observed in Europe than in North America, even during the global financial crisis of 2008 –2009. This point is well illustrated by Figure 2, which compares responsiveness of unemployment to output fluctuations in the United States and in France, in accordance with Okun’s law (where Y is output, k is full-employment growth rate, u is unemployment rate, ß is a coefficient and ε is the random term).

In addition to the varying degrees of labour market flexibility, somewhat different job preservation strategies adopted by the OECD countries played an important role in shaping varying employment trends. Virtually all these countries have adopted some measures to protect employment as part of their stimulus packages in addition to providing direct income support to the population and expanding unemployment benefits. However, in the United States, the relief policies did not aim at preserving the established employer-employee relationships to the same extent as in many European countries. In the United States, 27 States operate Short-Time Compensation (STC) programmes, funded by the federal government through the Coronavirus Aid, Relief, and Economic Security Act (CARES).

The incentives for employers provided by those programmes turned out to be insufficient to have a tangible effect (in particular, they remained liable for paying social security contributions). The programmes also imposed tough restrictions and involved administrative hurdles. At the federal level, the Paycheck Protection Program (PPP), designed to provide low-cost loans for small businesses to avoid layoffs, handed out around $520 billion in loans to around 5,000 businesses and is credited for saving millions of jobs within three months of its launch.7 Yet, the implementation of the PPP encountered numerous obstacles, as many loan applications were rejected by participating private lenders and businesses preferred to receive grants rather than loans, and the loan-to-grant conversion principles were opaque and complicated. Besides, only businesses employing fewer than 500 people were generally eligible to apply for these loans, leaving most of the workforce disqualified.

By contrast, many other OECD countries, including Australia, Canada, Denmark, the Baltic States, Hungary, the Netherlands, New Zealand, and the United Kingdom have introduced more explicit job retention schemes, especially for small and mediumsized businesses, in particular by introducing or expanding the coverage of existing short-time work schemes (subsidizing hours not worked) or introducing wage subsidies (in case of full-time employment). Japan expanded the coverage and eased the requirements for access to the Employment Adjustment Subsidy, increasing the subsidy rates for hours not worked to a maximum of 100 per cent for SMEs and introduced a new scheme covering SME workers who have remained without support because their employers have not applied for the subsidy. The Republic of Korea expanded its existing programmes, and subsidized employers’ costs of the shift to telecommuting. Some examples of those policies are shown below in Table 1. It is important to note that for those countries that experienced the sharpest rise in unemployment, its social costs may be aggravated by the break-up of an employee’s relationship with their company, which may complicate the return of these economies to full capacity, when the crisis is over.

By contrast, many other OECD countries, including Australia, Canada, Denmark, the Baltic States, Hungary, the Netherlands, New Zealand, and the United Kingdom have introduced more explicit job retention schemes, especially for small and mediumsized businesses, in particular by introducing or expanding the coverage of existing short-time work schemes (subsidizing hours not worked) or introducing wage subsidies (in case of full-time employment). Japan expanded the coverage and eased the requirements for access to the Employment Adjustment Subsidy, increasing the subsidy rates for hours not worked to a maximum of 100 per cent for SMEs and introduced a new scheme covering SME workers who have remained without support because their employers have not applied for the subsidy. The Republic of Korea expanded its existing programmes, and subsidized employers’ costs of the shift to telecommuting. Some examples of those policies are shown below in Table 1. It is important to note that for those countries that experienced the sharpest rise in unemployment, its social costs may be aggravated by the break-up of an employee’s relationship with their company, which may complicate the return of these economies to full capacity, when the crisis is over.

Some employment recovery observed, but long-run challenges are looming

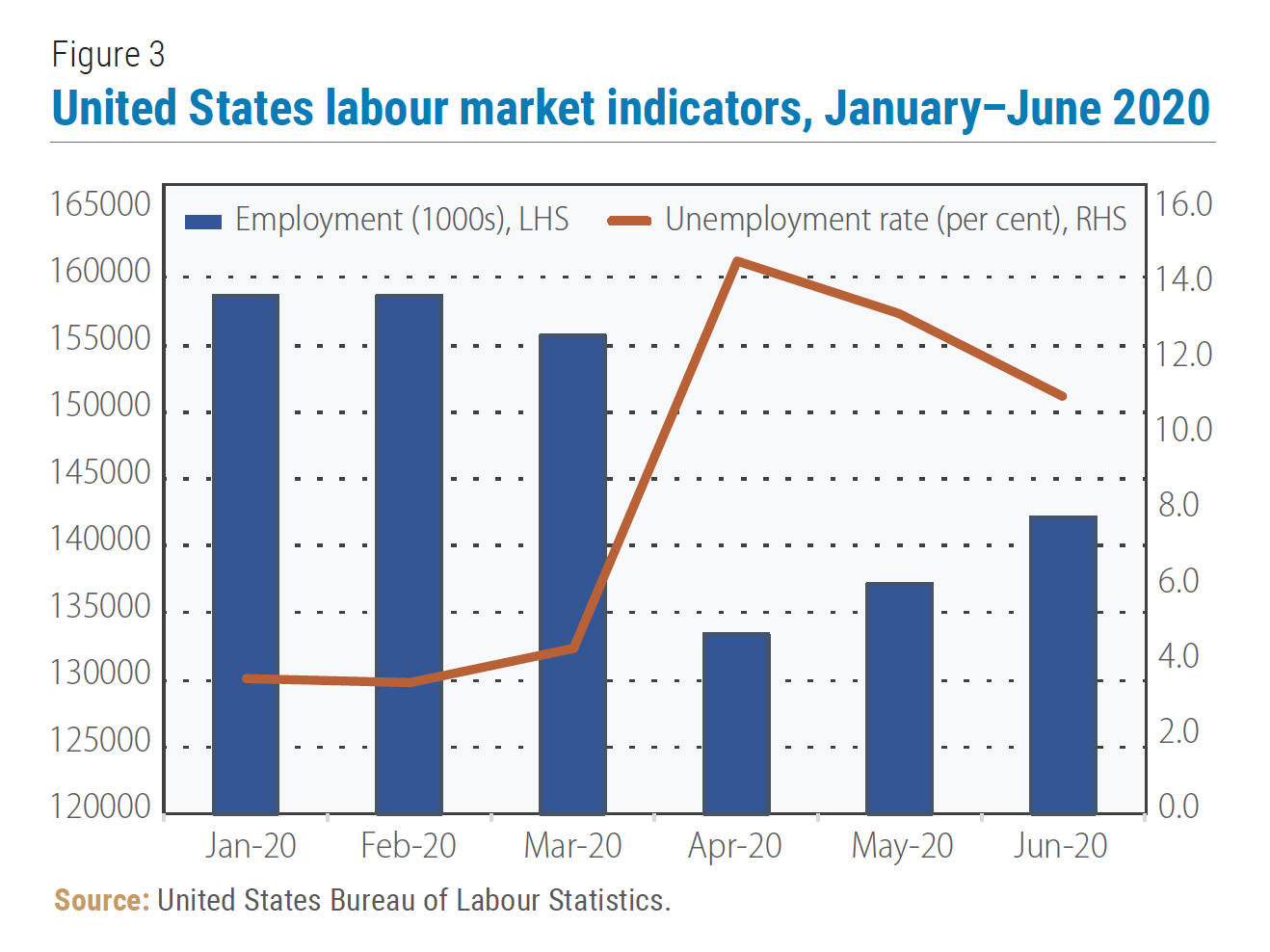

In May 2020 the aggregate unemployment rate in the OECD edged down to 8.4 per cent and according to preliminary data further declined in June, as the countries started a gradual reopening of their economies, and businesses started to recall workers. In the United States, which experienced the sharpest rise in unemployment among the OECD countries, labour market conditions somewhat improved (Figure 3), as the economy started to reopen and some of the earlier furloughed workers returned to work. Total civilian nonfarm payroll employment in June rose by 4.8 million and the unemployment rate declined to 11.1 per cent. Notable job gains were recorded in many sectors, including manufacturing, leisure and hospitality, retail trade, education and health services, and professional and business services. Nevertheless, the unemployment rate in the United States remained almost 8 percentage points above its pre-pandemic level. In July, as COVID-19 cases resurged across the country and reopening was paused or even reversed in 22 States, the speed of employment recovery has slowed. The Canadian economy added nearly one million jobs in June, as businesses started to reopen, and the unemployment rate dropped to 12.3 per cent from 13.7 observed in May. In Asia, the unemployment rate declined in the Republic of Korea in May, however it continued to climb in Japan. Meanwhile, despite the relatively successful efforts to protect jobs in Europe, although the unemployment rate in Germany in June increased more slowly than in April–May, it still did not reverse the trend, which may imply that the labour market is still adjusting to the lockdown effects, with some lag.

However, despite some short-term improvements, there are significant challenges ahead. Although under the current circumstances it is extremely difficult to make any projections of future employment trends in the OECD countries, it is important to differentiate between the short-term, cyclical impact of the pandemic on labour market conditions, which was alleviated by the massive stimulus programmes, and its longer-run consequences, which are likely to involve significant changes in the sectoral demand for labour, causing (in the best-case scenario) the relocation of workers across industries. The currently observed partial recovery in employment in some OECD countries in parallel with the gradual reopening of their economies and re-hiring of workers is to a large extent supported by the fiscal stimulus measures, which are set to expire soon. Despite the strong rebound in consumer confidence and retail sales in the United States in June, it is premature to talk about a sustainable recovery in aggregate demand. In Europe, the response of labour markets to the pandemic is still lagging, and the countries with low unemployment levels may not be able to sustain them when the wage support policies end. According to the OECD Employment Outlook 2020, even in the optimistic scenario of avoiding the second wave of infections under the pandemic, the OECD-wide unemployment rate may reach 9.4 per cent in the fourth quarter of 2020, exceeding all values observed since the Great Depression.

More serious challenges are emerging in the longer run. Numerous companies across all sectors of the economy, both in developed and in developing countries, may face bankruptcies and liquidation. Many subsidized sectors delivering public goods, including municipal services and public education, may face financial unsustainability. Even under the assumption of a prompt development of an effective vaccine and mass immunisation, there will be significant changes to the established ways of doing business— many major companies, including the large tech giants and the leading financial sector companies, have announced a massive shift to the broader use of telecommuting by their employees. The resulting decline in the need for office space will heavily impact commercial real estate development and hit the construction sector, which remains the driving force for some economies. Catering services in many cities will face lack of customers because of reduced office occupancy. The tourism and hospitality sectors will take a very long time—possibly years—to recover. Both leisure and business-related travel will remain supressed, especially as online meetings increasingly replace face-to-face interactions. As a result, several major airlines announced that they may drastically shrink their workforce, while aircraft production and avionics industries will also face a difficult period.

The current crisis is likely to accelerate the process of digitization and robotization, which was already going on for years in many industries, including automotive, electronics, warehouse management, and retail sales, both to minimize human interactions where social distancing requirements are difficult to meet, and to save on labour costs. This will have an adverse effect on medium-skilled jobs, and significant overall impacts on labour markets. The pandemic has also severely disrupted the functioning of the international trading system. Changes to the system of global supply chains and other aspects of global trade will cause shifts in employment patterns and unemployment rates in different countries. In the medium-term, not only the headline unemployment rates may persistently stand above their historical trend levels, but structural unemployment may become an entrenched problem. Such developments would tend to reinforce the trend to widening income and wealth inequalities.

More proactive labour market policies are needed

The COVID-19 crisis created unprecedented challenges for economic policymakers along all policy dimensions. The current recession is very different from the regularly observed routine dips in a business cycle and the conventional macroeconomic policies aimed at revitalising aggregate demand through monetary or fiscal stimulus will be insufficient in overcoming its consequences, especially in facilitating recovery in labour markets. Addressing such issues as long-term and structural unemployment will become a daunting policy challenge, in an already complex environment. During the last decades, because of technological changes and deepening globalization, labour markets around the world have become more dynamic, with increased worker mobility and new non-standard forms of employment. Currently, the COVID-19 pandemic will create new challenges. The deregulation of labour market has often been suggested as the most appropriate model, allowing to adapt to the new realities more efficiently. One may also argue that there is no need to protect jobs in sectors that are going to shrink drastically or eventually disappear in the aftermath of the pandemic. The United States model is often being cited as an example, with high labour mobility and generally quick post-recession recovery in employment. However, even in the United States, labour mobility has noticeably declined since 2010. As elsewhere in the OECD area, the age composition of the United States workforce has also been changing since the 1990s, with the share of older workers that are less flexible to adapt to new realities continuously increasing. Labour mobility remains relatively low in the EU, including geographic mobility of people, despite the common labour market for all EU member states. Flexibility and deregulation without pro-active government policies may lead to protracted high unemployment, especially among the new entrants to the labour force and the most vulnerable segments of the population. To overcome the COVID-19 related crisis, many countries have adopted stimulus measures of unprecedented scale, and active labour market policies can be well integrated into those policy packages. Such polices may include training in new technical skills required by the modernized production sectors, matching employees with prospective employers, subsidies or tax breaks to businesses hiring new employees, or publicly administered projects, in particular in building a greener economy. By contrast, failure to address the looming labour market problems may lead to a sharp increase in structural unemployment, complicating the reintegration of workers into the production process. It may also lead to an increase in the number of discouraged workers remaining outside of the labour force, putting additional burden on social welfare systems, dampening growth in potential output and slowing economic recovery.

Follow Us