Africa braces for global shockwaves

Africa braces for global shockwaves

Growth slows, but Africa’s economies are now more resilient

From Africa Renewal:

Reuters / Radu Sigheti

A trader on the Nairobi Stock Exchange: Since African capital markets are only marginally connected to world financial markets, the continent has not experienced stock crashes as severe as those in Northern economies.

A trader on the Nairobi Stock Exchange: Since African capital markets are only marginally connected to world financial markets, the continent has not experienced stock crashes as severe as those in Northern economies.Photograph: Reuters / Radu Sigheti

When several US investment houses collapsed in September, unleashing a chain of crashes in major markets around the world, brokers at Kenya’s Nairobi Stock Exchange anxiously watched the listings on their own boards. As feared, Nairobi share values did drop, and by late October were down 18 per cent from the start of the year. But that decline was far less steep than those in New York, London, Tokyo and other global financial centres.

The limited impact prompted Nairobi Stock Exchange Chairman James Wangunyu to explain that “the low level of development of our market and its minor presence in the global context has ensured that Kenya does not suffer a direct contagion effect.” But about the wider economy Mr. Wangunyu was less optimistic: “Kenya is part of an increasingly integrated global economy and the effects of the financial system turmoil in the United States and Europe is bound to have an effect, albeit a lagged one.”

For some Kenyans, there has been no lag at all. In the wake of political violence at the start of the year, Esther Kangogo has been struggling to recover from the damage to her Rift Valley home. For months, a daughter working in Texas regularly sent her money to help. But now, with harder economic times in the US, Ms. Kangogo told the UK’s Financial Times, her daughter “can’t afford to send money back home.”

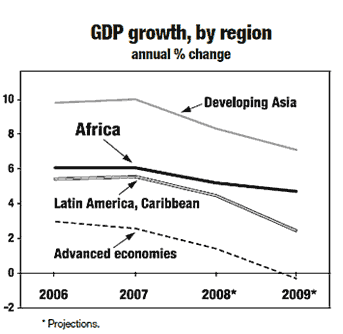

Source: UN Africa Renewal, from IMF forecasts, November 2008

Source: UN Africa Renewal, from IMF forecasts, November 2008As economic growth slows worldwide and some major industrial economies have gone into recession, it has become clearer that the repercussions of the global financial crisis will be felt throughout Africa’s “real economy” — beyond the narrow realm of stock trading. Dwindling financial remittances from Africans working abroad, lower world prices for Africa’s exports, scarcer and more costly commercial credit and less generous flows of foreign aid will inevitably dampen productive activity across the continent.

African ministers of finance and planning, meeting on 12 November, warned that the crisis “constitutes a major setback at a time when African economies were turning the corner.” The impact of the global financial crisis, in combination with high food prices, volatile oil markets and the repercussions of climate change will worsen conditions for millions of poor Africans. “We are facing a human as well as financial crisis.”

Flexibility and growth

While serious, Africa’s current economic situation is not as dire as it once might have been. Seven consecutive years of relatively high growth have allowed a number of countries to build up their monetary reserves and improve external financial balances, providing a cushion against short-term difficulties. In addition, economic reforms to enhance the productivity and efficiency of Africa’s farms, factories and markets have made its economies more resilient, notes Louis Kasekende, chief economist of the African Development Bank. “African economies have become more flexible than in the past,” Mr. Kasekende argues, “and are in a better position than before to absorb shocks.”

Exporting cocoa from Côte d’Ivoire: Recession in the world’s biggest economies has brought a slump in market prices for many of the primary commodities that Africa exports, thus hurting African incomes.

Exporting cocoa from Côte d’Ivoire: Recession in the world’s biggest economies has brought a slump in market prices for many of the primary commodities that Africa exports, thus hurting African incomes.Photograph: Reuters / Thierry Gouegnon

On 6 November, the International Monetary Fund (IMF) released updated forecasts showing that economic growth in all regions will slow markedly. But Africa’s performance will still be relatively strong, with 5.2 per cent average growth in gross domestic product (GDP) projected for 2008 and 4.7 per cent for 2009. That compares favourably not only to the hard-hit industrialized economies, but also to the growth rates of some other developing regions, such as Latin America and the Caribbean (see graph).

On 1 December, the UN’s Department of Economic and Social Affairs (DESA) released somewhat gloomier projections, showing even slower growth worldwide. According to DESA, Africa’s GDP growth will likely decline from 5.1 per cent in 2008 to 4.1 per cent in 2009. But that will still be higher than in Latin America and will stand in stark contrast to the dismal prospects for developed nations. In DESA’s best-case scenario there will be virtually no growth in the economies of rich countries in 2009, but they will more probably contract by 0.5 per cent, and perhaps by as much as 1.5 per cent.

One reason the global turmoil will have a less severe impact in Africa is that capital controls, good banking supervision and strong financial regulation have kept the continent’s banks focused on domestic deposits and relatively secure investments. They therefore had little exposure to the sub-prime mortgages and other dubious loans that brought down banks in the US and Europe. South Africa’s financial discipline, commented Jacob Zuma, head of the ruling African National Congress, has served as something of a “shock absorber” against the global crisis.

For many poorer African countries in particular, extensive debt write-offs in recent years have contributed to stronger balance sheets. The continent’s total official debt fell to $144.5 bn in 2007 (from $205.7 bn in 1999). Because these countries now do not have to spend nearly as much on servicing foreign debt, they have more left for strengthening social services and productive capacities.

Another factor is that Africa’s economies are somewhat less dependent than before on external markets and financing. Previously, says Razia Khan, the head of Africa research for the UK’s Standard Chartered bank, slowing world growth brought comparable slowdowns in African economies, mainly by weakening sales of the primary commodities that Africa exports. But now “we have noted that [Africa’s] growth is also fed by domestic consumption.” Luc Rigouzzo, director-general of Proparco, the investment arm of France’s aid agency, agrees, adding that rising domestic consumption has been driven by an increasingly urbanized population.

Commodity gyrations

The sources of African economic growth may now be more diverse, but the continent still relies heavily on sales of oil, minerals, coffee and other raw materials. Exports of Africa’s beverage crops, such as cocoa and coffee from Côte d’Ivoire or tea from Kenya, are typically sensitive to downturns in US and European markets. A number of African countries have benefited in recent years from robust sales of clothing and textiles to the US under the favourable market-access provisions of that country’s Africa Growth and Opportunity Act, but those too may be in jeopardy as US consumers buy fewer goods.

World prices of metals, which have been relatively high for several years, have fallen especially sharply. During October alone the price of copper, Zambia’s major export, plunged by a steep 37 per cent. Silver was down by 21 per cent and even gold — often a refuge for investors in troubled times — came down 18 per cent.

BHP Billiton, the world’s third largest producer of nickel, has suspended its nickel prospecting in the North Katanga region of the Democratic Republic of the Congo (DRC), because of the slide in nickel’s price. Jean-Félix Mupande, director-general of the DRC’s mine-registration agency, also worries about slowing economic growth in China. “Congo’s mining sector, which is tied closely to China, will certainly feel the blow,” he says.

In Burkina Faso, Prime Minister Tertius Zongo presided over the inauguration of a new gold mine in early November. But work on other mining projects, he noted, has been delayed by mining companies’ difficulties in raising commercial financing. “Those who think that the international financial crisis will not have an impact on our countries are making a very simplistic analysis,” Mr. Zongo commented. Burkina, which had already been hit by low world prices for cotton, historically its major export, was counting on the opening of several new gold mines to boost its fortunes.

Although mining accounts for only 5 per cent of South Africa’s economy, that country has been hit especially hard by the mining slump, in part because its well-developed stock exchange is closely integrated into international capital markets and foreign investors can dump their holdings relatively easily. By the end of October foreigners had sold a net 48 bn rands (US$6.1 bn) of local stocks since the beginning of the year, compared with a net acquisition of R62 bn for the same 10-month period the year before.

However, the South African government is used to the mining sector’s “nasty tendency to boom and bust,” Finance Minister Trevor Manuel said in October. “Whether you can smooth out the gyrations is the test of the quality of fiscal policy.” Because the government spent cautiously during the years of high mineral prices, he explained, it is now in a better position to weather the current storm.

Oil and food

For a number of major African oil producers, such as Nigeria, Angola and Algeria, high world oil prices delivered a boom in foreign earnings. But as global demand for oil slackened, its price fell by more than half in just three months, upending expenditure plans that were based on much higher prices. Even if oil-exporting countries reduce production, the IMF projects that through 2009 oil prices will remain only moderately higher than their current levels.

For Africa’s many poor oil-importing countries, that is good news. They will not have to spend as much of their scarce money on costly fuel imports, leaving more for domestic investment and other purposes.

Many of these countries were also hit hard by high prices for imported cereals during the first months of 2008, setting off widespread protests and rioting by hungry citizens (see Africa Renewal, July 2008). Although world grain production has been strong, contributing to a slight fall-off in international prices, those lower prices have not yet been felt by consumers in Africa’s poor food-importing countries, the UN’s Food and Agriculture Organization (FAO) noted in November in its biannual Food Outlook report.

And because of the current global economic uncertainties, many farmers in major food exporting countries elsewhere in the world may reduce their plantings, warns Concepción Calpe, one of the FAO report’s main authors. “There is a real risk that as a consequence of the current world economic problems people will have to reduce their food intake and the number of hungry could rise further,” she says.

Aid in jeopardy?

Photograph: Associated Press/ Dominic Lipinsky

Photograph: Associated Press/ Dominic Lipinsky

Kenyan Prime Minister Raila Odinga:“As the economies of our main donor partners are affected, the first victim is going to be aid.”

On 22 September, just as the Wall Street crash began spreading worldwide, the UN General Assembly held a high-level meeting in New York on Africa’s development needs. Leaders from Africa appealed to donors to live up to their earlier pledges to significantly increase foreign aid to Africa, and many of the rich donor countries reaffirmed their commitment to do so (see article and Africa Renewal, October 2008).

As the crisis worsened, many African leaders voiced concerns. “We fear,” said Kenyan Prime Minister Raila Odinga, “that as the economies of our main donor partners are affected, the first victim is going to be aid.... We know that they must look at some areas where they will make some savings, and we fear the first area will be development assistance.”

Such concerns were bluntly reinforced by French Foreign Minister Bernard Kouchner. Commenting on donor pledges to increase aid to help poor countries achieve the Millennium Development Goals, he repeatedly stated in New York in late September, “Promising to get people more money for development? This is not true. We are lying.”

A month later a French non-governmental group, the Comité catholique contre la faim et pour le développement–Terre Solidaire (CCFD), warned that French officials were considering cutting aid payment authorizations in the 2009 budget by more than half. In a subsequent meeting with the CCFD and other French charities, Alain Joyandet, secretary of state for cooperation, denied that such drastic cuts were envisioned and vowed that most of France’s health and education projects in sub-Saharan Africa would be maintained.

On the eve of an international conference on “financing for development” in Doha, Qatar, on 29 November–2 December, UN Secretary-General Ban Ki-moon noted, “The vast sums committed to bailing out banks and private companies dwarf ODA [official development assistance]. Surely we can find the much more modest amounts needed to sustain more than a billion lives.” At the conference, donor countries did in fact reaffirm their commitments to increase aid to the poorest countries.

Remittances stall

Private financial flows to Africa have also been affected. Migrant remittances — the money sent home by those working abroad — had been growing rapidly in recent years, reports Hania Zlotnik, director of the population division of the UN’s Department of Economic and Social Affairs. Citing World Bank data, she notes that remittances to all developing countries increased by an average of 17 per cent annually between 2002 and 2006, although in 2007 the growth in remittances slowed to around 10 per cent.

Now anecdotal evidence from a number of African countries, such as Senegal and Kenya, suggests that such flows are declining significantly. In 2007 Kenya received about $1.3 bn in remittances, more than it normally gets in foreign aid. But in August remittances were already 38 per cent lower than during the same month the year before. With between 750,000 and 1 million Kenyans working in the US and another 200,000 in the UK, rising unemployment in those economies will make it even harder to send money to relatives back home.

In France many African migrant labourers are employed in construction. But some industry executives predicted in October that as many as 180,000 building jobs may be lost in that country.

‘Credit crunch’

Commercial credit has also become scarcer — and thus more costly. Across Africa, governments and local companies have been gearing up to build and improve roads, railways, ports and other infrastructure vital for the continent’s development (see article). While some funds have been from public sources, including governments and the African Development Bank and World Bank, the bigger projects have typically entailed some commercial borrowing as well.

When the South African government wants to build a new toll road or purchase locomotives for its railways, notes Tom Boardman, the chief executive officer of that country’s Nedbank, it usually goes to US or Japanese banks. “Now,” he explains, “these international banks aren’t lending anymore, so I’m not sure South Africa will be able to get all the funding it needs.”

South African authorities remain determined to continue their ambitious infrastructure development plans — in part to help stimulate the domestic economy — and indicate that they will seek to raise more of the needed financing from local banks than before. But the international “credit crunch” means that all borrowing will be more expensive — adding to the future debt burdens that South Africa and other countries will be obliged to take on.

Foreign investment

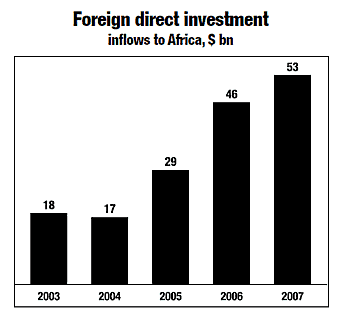

As a percentage of all foreign direct investment (FDI) globally, Africa’s share (3 per cent) has remained the lowest in the world. But in absolute terms the value of such flows to Africa is significant, and has been rising sharply. According to estimates by the UN Conference on Trade and Development (UNCTAD), Africa’s inflows of FDI jumped from just $17–18 bn in 2003–04 to $53 bn in 2007, their highest level ever (see graph, below).

Source: UN Africa Renewal, from data in UNCTAD, World Investment Report 2006, 2008

Source: UN Africa Renewal, from data in UNCTAD, World Investment Report 2006, 2008Much of this surge was a result of the commodities boom, UNCTAD notes in its World Investment Report 2008, released in September. Oil producers, which traditionally have received most new foreign investments in Africa, remained the greatest beneficiaries. But, emphasizes UNCTAD, other countries also attracted investors to their financial services and telecommunications sectors, new mining projects and, to a lesser extent, manufacturing. Africa’s least developed countries accounted for more than $10 bn of FDI inflows in 2007.

A number of African analysts worry that the global crisis will seriously weaken foreign investment in Africa, and work on new mining projects in a number of countries has already been delayed. Mozambique’s Foreign Minister Oldemiro Baloi fears that a global recession will lead foreign investment to his country to “dry up.” In October, the Ghana Investment Promotion Centre warned that the last quarter of 2008 will likely be “tough” for that country’s investment climate.

On the bright side, however, Africa has some advantages to offer. According to UNCTAD, the rates of return on foreign investments in the continent were the highest of any developing region’s in 2006 and 2007. By improving their policies and investment climate, a number of governments have also succeeded in countering common investor perceptions that Africa is a poor gamble because of its political insecurity, high rates of disease and limited infrastructure.

With the prospects in many of the world’s more advanced “emerging markets” now increasingly volatile and uncertain, some investors are starting to look at Africa in a new light, analysts report. Africa no longer seems such a risky bet.

Podcast