UN DESA | DPAD | Development Policy Analysis Division

** This page has moved permanently. If you are not redirected please click here: https://www.un.org/development/desa/dpad/document_gem/global-economic-monitoring-unit/monthly-briefing-on-the-world-economic-situation-and-prospects/ **

World Economic Situation and Prospects

Monthly Briefing

9 January 2017 Summary

- Rates of return in the United States rise relative to the rest of the world

- European Union sanctions against the Russian Federation extended

- Recent improvement in East Asia’s exports could see setback amid significant uncertainties

Global issues

Rates of return in the United States rise relative to the rest of the world

The Federal Open Market Committee (FOMC) of the United States Federal Reserve (Fed) raised the target range for the federal funds rate by 25 basis points on 15 December, a move that was widely anticipated by financial markets and economic forecasters. This marks the second interest rate move by the Fed since rates were reduced to near-zero levels at the height of the financial crisis in December 2008, and the only monetary policy change in the United States of America in 2016. The FOMC based this decision on evidence of further improvements in the labour market, a moderate pace of economic expansion and an inflation trajectory that is expected to rise to 2 per cent as the transitory effects of past declines in energy and import prices dissipate. Despite this increase, financial conditions in the United States remain accommodative, and the size of the Fed’s balance sheet will remain at current levels until the normalization of the level of the federal funds rate is well under way.

The Fed’s move followed shortly after an announcement on 8 December of an extension of the quantitative easing programme of the European Central Bank (ECB). The ECB will extend its monthly purchases under its asset purchase programme until at least the end of 2017, although tapering the pace of expansion to €60 billion per month from €80 billion per month starting in April 2017. Meanwhile, the Bank of Japan (BoJ) unveiled a new set of unconventional monetary policy measures in September, aimed at boosting inflation and reviving growth. The divergence in monetary policy stances of the major central banks, although widely anticipated and largely priced into global financial markets, nonetheless impacts global exchange rates and the direction of capital flows.

The interest rate increase by the Fed entails a rise in debt-servicing costs, both domestically and in the many developing economies and economies in transition that have exchange rates closely linked to the United States dollar or hold debt denominated in dollars. In line with the United States, several economies increased policy rates in December. This included Bahrain, Hong Kong Special Administrative Region of China, Kuwait, Qatar, Saudi Arabia, United Arab Emirates and countries in the West African Economic and Monetary Union. Meanwhile, Mexico increased rates by 50 basis points, bringing the cumulative rise in the policy rate to 250 basis points in 2016. Likewise, Turkey increased rates in November, in response to rising exchange rate pressures.

Global exchange rates and financial markets have shifted significantly since the presidential election in the United States in November. The outcome of the election has led many investors to expect a change in the country’s macroeconomic policy mix in the coming months, with a shift towards looser fiscal and tighter monetary policy. These expectations are consistent with the views expressed by the participants of the FOMC on the appropriate level of the federal funds rate going forward. The median forecast is currently for a cumulative 75 basis point rise in the federal funds rate by end-2017. This compares to forecasts for a cumulative 50 basis point rise at the FOMC meeting in September 2016, prior to the election.

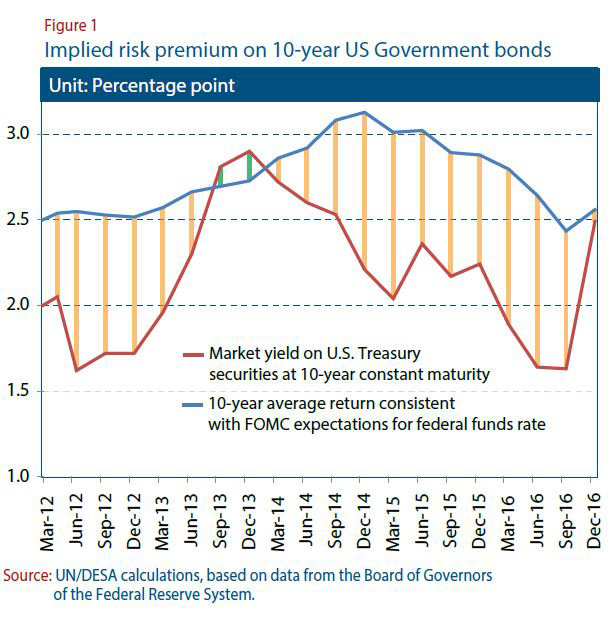

Except for a brief period in late-2013, financial markets have consistently priced in a slower rise in United States’ policy rates compared to the expectations expressed by the participants of the FOMC, offering a significant negative term premium on the market yields on government bonds since 2012 (figure 1). This term premium has essentially disappeared since the presidential election in the United States in November 2016, and Government bond yields are now more closely aligned with the expected path of the federal funds rate, reflecting a sharp rise in bond yields.

The market yield on 10-year Government bonds in the United States has risen by about 60 basis points since the presidential election, signaling both a faster pace of interest rates rises by the Fed and a rise in Government borrowing costs. The rise in bond yields may reflect expectations that the new Administration in the United States will shift towards a significantly looser fiscal stance, entailing a rise in the deficit and a rise in Government debt. While there remains considerable uncertainty about the specific measures that will be introduced, proposals include a large expansion of infrastructure investment and significant tax cuts, especially for corporations.

Certain types of capital flows may respond more directly to Government bond spreads than to differentials in policy interest rates, as Government bonds are themselves investment instruments. Bond yields have risen in most major countries since November, with a few exceptions such as Greece, India and the Russian Federation, where country-specific factors have dominated movements in bond yields. However, rates of return have declined in most countries relative to the United States, especially after adjusting for exchange rate depreciations, which lower the rate of return to foreign investors. Figure 2 illustrates the change in 10-year Government bond yields relative to that in the United States since 5 November, after adjusting for exchange rate movements against the US dollar. In the sample of major developed, developing and transition economies shown, all – with the exception of the Philippines – have seen a decline in return relative to the United States. This can be expected to shift some capital flows towards United States’ assets. This impact is already apparent, as emerging market economies experienced the largest recorded weekly outflows from bond funds in the week following the election in the United States.

Developed economies

Canada: provinces show support for a national carbon price

Canada continues to make important strides in its climate policy, demonstrating concerted efforts to meet its obligation under the Paris Agreement of cutting emissions by 30 per cent from 2005 levels by 2030. In September 2016, the Government announced a major infrastructure investment plan that explicitly highlights support for infrastructure projects that reduce greenhouse gas emissions. In November 2016, the Government committed to phasing out coal-generated electricity by 2030. Most recently, in December 2016, Canada’s prime minister and 11 of Canada’s 13 provincial and territorial leaders announced that they had agreed on a national climate framework, which includes introducing a carbon tax or cap-and-trade scheme by 2018. Each province will introduce a scheme that puts a minimum carbon price of 10 Canadian dollars (Can$) per tonne by 2018, rising by Can$ 10 per year to reach Can$ 50 per tonne by 2022. Provincial governments will have full control over how the revenues raised by the scheme are used, which may include, for example, rebates to offset the impact of the tax on lower- and middle-income households or other disadvantaged sectors.

Several of Canada’s provinces and territories have already made important steps towards a carbon pricing scheme. British Columbia introduced a carbon tax in 2008, which currently stands at Can$ 30 per tonne. Alberta introduced a carbon levy starting 1 January 2017, of Can$ 20 per tonne, rising to Can$ 30 per tonne on 1 January 2018. Québec introduced a cap-and-trade system in 2013, and Ontario will hold its first official cap-and-trade auction in March 2017. Nova Scotia has already reduced greenhouse gas emissions by 30 per cent of 2005 levels, largely as a result of a transition away from coal-fired power generation. The government of Saskatchewan has not yet agreed to a national carbon price, citing concerns related to the impact on energy, mining and agricultural industries in particular, and more broadly on the competitiveness of Canadian firms if carbon policy diverges significantly from that in the United States, Canada’s largest trading partner and most important economic competitor.

Europe: rising inflationary pressures in several countries

Inflation rates have been rising in a number of European economies. In the United Kingdom, consumer prices increased by 1.2 per cent in November, the fastest increase in more than two years. All non-food categories contributed to the price increase and while inflation still remains below the central bank’s target level of 2 per cent, further upward price pressures are expected due to the recovery in oil prices and higher import costs given the depreciation of the British pound sterling. Likewise, in Finland, inflation picked up to 0.7 per cent in November, the fastest rate in two years. The strong performance of the real estate market remains a major driving force behind the acceleration in inflation, with house prices increasing by 3.1 per cent in the third quarter. In the euro area as a whole, inflation rose to 1.1 per cent in December, breaching 1 per cent for the first time since September 2013. This overall picture of increasing inflation is accompanied by rising growth and continued labour market improvements in some countries. For example, in the Netherlands, unemployment stood at 5.6 per cent in November, down from 6.7 per cent a year earlier. Employment increased by 2.5 per cent and nominal wages have also shown a more solid upward trend, increasing by about 2 per cent.

Economies in transition

European Union sanctions against the Russian Federation extended

In December, the European Union extended its economic sanctions against the Russian Federation for another six months. Initially introduced in July 2014, these sanctions, among others, involve limiting the access of a number of Russian financial institutions and companies to European capital markets, as well as restricting access to certain technologies, including those related to oil exploration and production. The Russian economy has nevertheless adjusted to the sanctions environment and is expected to return to a moderate growth path in 2017. Forward-looking purchasing managers’ index (PMI) indicators reached multi-year record levels in December. According to preliminary estimates, annual inflation in the Russian Federation in 2016 dropped to 5.4 per cent – the lowest level in 25 years, since the beginning of economic transformation.

Nevertheless, the external environment remains challenging for most of the economies of the Commonwealth of Independent States. In Belarus, GDP contracted by 2.8 per cent in the January-October period, in part because of the low capacity utilization of oil refineries – the major source of foreign exchange revenue, while the stock of bank credit fell. In the Caucasus, the Armenian economy declined by 2.3 per cent in the third quarter, following two quarters of growth. Meanwhile, the economy of Azerbaijan is estimated to have contracted by 3.9 per cent in January-November. On the monetary policy front, in December, the Central Bank of Armenia cut its policy rate by 25 basis points to 6.25 per cent, amid slowing inflation and relatively lower currency volatility. During the month, the National Bank of Kyrgyzstan also reduced its policy rate by 50 basis points to 5 per cent, bringing the cumulative decline in the policy rate to 500 basis points in 2016. In contrast, inflation accelerated in Ukraine, putting pressure on the exchange rate and reversing the trend of the first half of 2016, mostly due to higher utility tariffs.

In South-Eastern Europe, Serbia’s GDP growth in 2016 is preliminarily estimated at 2.7 per cent, considerably higher than the 0.8 per cent recorded in 2015. Despite the fiscal consolidation policy restraining domestic demand, the economy was boosted by lower production costs associated with lower energy prices and by stronger export demand form the regional trade partners. An ample harvest has also led to an 8 per cent increase in agricultural output. In the former Yugoslav Republic of Macedonia, third quarter GDP increased by only 2.4 per cent, as the country moved to a lower-growth trajectory, due in part to internal political tensions and base year effects.

Developing Economies

Africa: subdued growth in South Africa amid growing fiscal concerns

Recent economic indicators continue to point towards a subdued growth outlook for South Africa. In the third quarter, the economy’s growth momentum slowed from 3.5 per cent to 0.2 per cent on a quarter-on-quarter annualized basis, mainly due to a sharp decline in manufacturing activity. The weakness in the manufacturing sector also extended into the fourth quarter, as factory output fell in October, while the manufacturing PMI index contracted in November.

Looking ahead, the recent upward trend in commodity prices will support a modest growth recovery in South Africa. Nevertheless, the economy continues to be buffeted by several external and domestic headwinds. Sluggish global demand has contributed to a worsening of South Africa’s external position. In the third quarter, the current account deficit widened to 4.3 per cent of GDP, as export volumes declined. In addition, elevated global uncertainty is generating high capital flow and currency volatility, dampening investor sentiments. On the domestic front, structural issues continue to weigh on private consumption and investment activity. Of note, unemployment reached a 13-year high of 27.1 per cent in the third quarter, amid weak job creation and high skills mismatch. Increased political and policy uncertainty has also resulted in deterioration in the domestic investment environment.

Weak economic growth in South Africa has contributed to a worsening of its fiscal position. In 2016, public debt is estimated to have risen above 50 per cent of GDP, fueling concerns over a potential sovereign rating downgrade to sub-investment grade. Against this backdrop, policy makers are facing the difficult task of balancing between preserving fiscal sustainability while supporting growth and development prospects.

East Asia: recent improvement in exports could see setback amid significant uncertainties

East Asia is witnessing signs of improvement from the export slump that has plagued the region since late 2014. In United States dollar terms, all major trading economies in the region have experienced negative year-on-year growth in nominal merchandise exports for most of the 24 months leading up to October 2016. However, the trend has improved over the course of 2016, with the aggregate nominal export growth of the region’s top five trading economies improved from -20.9 per cent in February 2016 to -4.8 per cent in October 2016. The improvement can be partly attributed to the rise in export prices, but available data also suggests a recovery in real exports.

It is however unclear whether the recent improvement in export growth can be sustained. Multiple factors, including tepid demand from major trading partners, ongoing structural changes in China’s import composition, and the steady rise in non-tariff measures imposed on goods from the region, have been contributing to the weak exports in recent years and could continue to impede export performance. Furthermore, possible changes in trade policy of the United States pose additional uncertainties. If adopted, a more restrictive trade stance of the new Administration of the United States toward China would have cascading effects on the rest of East Asia, given the centrality of China’s position in the regional value chain.

South Asia: Iran’s economy gains momentum

After several years of slow economic growth, Iran’s economy expanded vigorously by 7.4 per cent in the first half of the current fiscal year initiated last March. This positive economic performance can be attributed to the strong expansion of oil production and exports, improving business and consumer confidence, and a surge in foreign investments. In the first nine months of 2016, oil production increased by almost 20 per cent compared to the same period in the previous year, reaching a new multi-year record of 3.7 million barrels per day in September. Moreover, oil production is projected to increase even further as Iran is not obligated to implement production cuts under the new agreement among members of the Organization of Petroleum Exporting Countries reached last November. Large oil companies also continue to actively explore new business opportunities in the energy sector. In addition, several Iranian companies have signed business contracts with Chinese and Indian firms in recent months, to upgrade oil refineries and to develop large infrastructure projects, including the Chabahar port, which signals favourable investment prospects in the near term. Importantly, the strong growth recovery has not only been confined to the oil sector, as non-oil activities grew by 4.5 per cent in the same period. Against this backdrop, Iran’s economy is projected to expand at a robust pace in 2017.

Western Asia: economic woes in Turkey prompt new measures to boost credit growth

In the third quarter, the Turkish economy unexpectedly shrank by 1.8 per cent on a year-on-year basis, following an expansion of 4.5 per cent in each of the two previous quarters. The slump in economic activity was driven by a visible fall in exports of goods and services and private consumption, amid a poor tourism season, a significant depreciation of the lira and lower investor and consumer confidence stemming from the failed military coup last July. In particular, exports fell by 9.2 per cent, while household spending declined by more than 3.0 per cent. In contrast, government expenditure increased strongly by 23.8 per cent. Given the recent sharp depreciation of the domestic currency and that consumer price inflation remains well above the central bank’s target, monetary policy is severely constrained to provide additional support to economic activity. Furthermore, in November, the central bank raised interest rates for the first time in almost three years. Against this backdrop, the Turkish Government announced a new set of policy measures to revive growth, with a main focus on increasing the availability of credit to the private sector. Notably, the government is creating a new $72 billion fund to provide credit lines for small- and medium-sized enterprises. Also, the state-owned Eximbank–Turkey’s official export credit agency–will offer zero interest rates on foreign exchange loans for Turkish multinational firms, particularly for their acquisitions of locally-made goods and services.

Latin America and the Caribbean: the monetary easing cycle in South America continues

Amid persistent economic weakness and ongoing disinflation, central banks in South America have continued to ease monetary policy. In December 2016, the Central Bank of Colombia reduced its policy rate by 25 basis points to 7.5 per cent after consumer price index (CPI) inflation declined faster than expected. Year-on-year inflation slowed to 6 per cent in November, down from 9 per cent in July 2016. The decline in inflationary pressures can be attributed to a fading impact of adverse supply shocks (associated, for example, with El Niño), a more stable domestic exchange rate and weak domestic demand. In the third quarter of 2016, Colombia’s GDP grew by only 1.2 per cent on a year-on-year basis, the slowest pace since early 2009. Domestic demand contracted by 1.1 per cent due to a significant decline in investment and a slowdown in private consumption. Chile’s central bank kept its main policy rate at 3.5 per cent in December, but shifted its outlook from neutral to an easing bias, anticipating rate cuts in early 2017. CPI inflation in Chile has fallen from 4.8 per cent in January 2016 to 2.9 per cent in November, slightly below the target rate of 3 per cent. Further easing in early 2017 is also expected in Argentina and Brazil, where policymakers are struggling to lift their economies out of recession. Argentina’s economy contracted more severely than expected in the third quarter of 2016. GDP fell by 3.8 per cent year-on-year as investment (especially in construction) plunged.