Emerging economies hold promise for Africa

Reuters / Antony Njuguna

Chinese-financed road construction project in Kenya: China, India, Brazil and other emerging market countries are especially active in developing Africa’s infrastructure.

Chinese-financed road construction project in Kenya: China, India, Brazil and other emerging market countries are especially active in developing Africa’s infrastructure.Photograph: Reuters / Antony Njuguna

In April South Africa’s largest clothing and textile manufacturer, Seardel, announced plans to close its Frame Textiles division. The company blamed competition from cheap imports — three-quarters of which come from China — as one of the reasons. The shutdown will add some 1,400 workers to the country’s growing ranks of unemployed, unless government-led efforts for a rescue plan are successful.

The following month Zambian President Rupiah Banda announced that China’s Non-Ferrous Metal Mining Company (NFC) had been awarded a contract to reopen the closed Luanshya Copper Mines, reinstating some 1,700 miners.

The two events highlight the pluses and minuses of Africa’s mushrooming economic ties with “emerging economies” like China. In the last three years Africa’s trade with China has doubled, reaching $106.7 bn in 2008. And while China dominates in terms of sheer numbers, trade and investment with other emerging markets, such as Brazil, India and Malaysia, has also been rising sharply in recent years.

African manufacturing has often felt the adverse impact of such trade, and there are fears over the “deindustrialization” of the textile industry, for example. But consumers have clearly benefited from the low-priced and easily available goods, ranging from sandals to trucks, which have flooded African shops and markets. Meanwhile, rising exports to emerging economies of oil, iron ore, cocoa and other commodities have boosted Africa’s earnings, and companies from Brazil, China, India and Russia are building more roads, hydropower plants and refineries across the continent.

Africa’s remarkable record of economic growth in recent years has to an important degree been underwritten by the explosive growth of countries like China, Martyn Davies, director of the Centre for Chinese Studies at South Africa’s Stellenbosch University, told Africa Renewal. With new markets in which to sell their goods and alternative sources of financing, African countries have been able to lower their dependence on traditional partners in Europe and the US (see Africa Renewal, October 2008).

But now the deepest world economic downturn since the Great Depression 80 years ago has dented Africa’s burgeoning economic links with its new markets. Export orders have plummeted and many Chinese- and Indian-owned businesses have shut down or have been forced to lay off workers.

Yet analysts are optimistic that the economic opportunities presented by emerging economies remain, albeit in less spectacular forms. And in a tougher and even more competitive economic environment, African governments and companies must play smart if they are to reap the full benefits.

Solidarity across the South: Indian Prime Minister Manmohan Singh, then South African President Kgalema Motlanthe and Brazilian President Luiz Inácio Lula da Silva, meeting in New Delhi in October 2008.

Solidarity across the South: Indian Prime Minister Manmohan Singh, then South African President Kgalema Motlanthe and Brazilian President Luiz Inácio Lula da Silva, meeting in New Delhi in October 2008.Photograph: Reuters

“Whilst some emerging economies have a strategy for Africa, Africa does not have a strategy towards the emerging economies,” says a recent report, Africa’s Cooperation with New and Emerging Development Partners: Options for Africa’s Development, prepared for the UN’s Office of the Special Adviser on Africa (OSAA). Having a strategic approach is vital, the paper says, because Africa is much less important to its new trading partners than they are to Africa.

Grounds for optimism

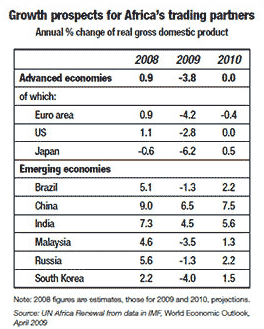

International Monetary Fund (IMF) projections for world growth reinforce the grounds for optimism. While many of Africa’s traditional trading partners are in a recession, many of its new markets, particularly China and India, show relatively healthy growth prospects (see table below).

The developed countries’ Organization for Economic Cooperation and Development (OECD), in its report Taking Stock of the Credit Crunch, argues that how well African and other poor countries withstand the present crisis depends more on the rest of the developing world than on prospects in Northern countries. If, as looks possible, growth continues in countries like China and India, “one long-term consequence of the current crisis may be an accelerated reconfiguration of the global economy in favour of the developing world.”

About one-third of Africa’s total trade is already with markets in emerging or other developing country, marking a shift away from the previously overwhelming reliance on its traditional trading partners. Although the European Union (EU) as a whole continues to dominate Africa’s trade, that dominance is receding, especially in imports: the EU now accounts for only a little over a third of the continent’s inward trade.

China alone is Africa’s second-largest single trading partner. So its economic activities can have a big impact. China’s recent decision to initiate a large-scale package of domestic stimulus measures has already begun to bear fruit, Zhang Yansheng, an analyst at China’s National Development and Reform Commission, told the national news agency, Xinhua, in May. According to the Ministry of Commerce, imports of oil and iron ore — two key African exports — rose in April.

Though the economic signals from China and other major emerging markets remain mixed, commodity markets have reflected the anticipation of increased demand with modest gains in the prices of oil, copper and other metals in April and May.

Political commitment

Such signs of economic buoyancy are being reinforced by renewed political commitment. Indian officials have reconfirmed the promises they originally made at an India-Africa Summit in April 2008. These include plans to provide $500 mn in grants over the next five to six years and to double lines of credit to $5.4 bn, towards a target of doubling India-Africa trade to $70 bn during this period. India also agreed to reduce tariffs on a wide range of imports from Africa, mainly agricultural products.

Store in Bamako, Mali: Cheap Asian imports are welcomed by African consumers, but can undercut domestic manufacturers.

Store in Bamako, Mali: Cheap Asian imports are welcomed by African consumers, but can undercut domestic manufacturers.Photograph: Alami Images/ dbimages

Chinese officials too have recently reconfirmed commitments made at the 2006 China-A frica Summit in Beijing to double aid to Africa and reduce barriers to its imports. In February, President Hua Jintao visited Mali, Mauritius, Senegal and Tanzania with a series of aid and loan packages. Lower-level officials have continued to deliver the message since then, with visits to Cape Verde, Eritrea, Ghana and Kenya. In November 2009 Egypt will host the fourth China-Africa Summit.

Mr. Davies is convinced that China will continue to strike more investment deals with African countries. The China Development Bank and China Import-Export Bank are actively considering a large number of commitments, he says, predicting a spate of Chinese investment in smaller mining operations to take advantage of current cheap prices. Pointing to the flight of Western private finance in recent months, he contrasts the “five-minutes-to-five-years time horizons” of Western investment banks with the 20-year strategic vision of Chinese investing institutions.

In March, in Johannesburg, the $5 bn China-Africa Development Fund (CADFund) opened its first office in Africa. At a time when much Western capital is fleeing the continent, the CADFund, established in 2007 by the state-owned China Development Bank as an equity investment fund for Africa, has already spent some $400 mn of its initial $1 bn capital and is reported to be adding a further $2 bn to help promote more Chinese investment in Africa.

The UN Conference on Trade and Development (UNCTAD) believes the investment flows from countries in the South will be maintained because of the good deals now available, while the OECD in its recent report on the global credit crunch likewise sees “some early signs that South-South investments may come out of the crisis strengthened over the long term.”

Focus on infrastructure

The impact of emerging economies is particularly noticeable in infrastructure. At Kilamba Kiaxi, on the outskirts of Luanda, Angola, Chinese companies are building a new township designed to accommodate some 200,000 people, complete with schools, business sites, access roads, sewage plants and other needed infrastructure. UNCTAD estimates that Southern-owned companies account for 40 per cent of all infrastructural commitments made in Africa between 1996 and 2006. According to the donor-led, World Bank-managed Public-Private Infrastructure Advisory Facility (PPIAF), China’s planned investment in hydroelectric schemes could increase Africa’s generating capacity by 30 per cent.

India has committed some $500 mn in infrastructure investments over the last five years, much of it in Nigeria, involving an oil refinery, power plant and railway, though project implementation still awaits the result of a feasibility study. Brazilian and Chinese construction companies have a long history in Angola, Mozambique, Tanzania and Zambia. In transport, India’s Tata has a well-established presence in Nigeria and South Africa, exporting assembled vehicles from there to other African countries. Russia has had a similarly long involvement in Angola and Guinea, and recently has been increasing its presence in Nigeria and South Africa.

Both partners and rivals

The rapidly growing telecommunications sector shows how complex some investment patterns have become. According to UNCTAD, Southern companies account for nearly 60 per cent of commitments in recent years. These include African-owned companies like South Africa’s MTN and Egypt’s Orascom, which dominate the markets in many countries. In an ever-changing sector, they are facing strong competition from other Southern-based companies, such as Kuwait’s Zain and China’s ZTE, as well as developed-country rivals like the UK’s Vodafone.

The complexity of Africa’s ties with emerging markets was highlighted by the announcement in May that South Africa’s MTN was in talks with Indian telecommunications giant Bharti about a share-exchange deal that would help to give both companies greater global clout. In 2007 China’s Industrial and Commercial Bank paid $5.5 bn for a 20 per cent stake in South Africa’s Standard Bank, which has affiliates in 17 African countries, as well as in Brazil and Russia. In the fight for global markets, African and emerging-market companies can be both partners and rivals.

Raw materials

Despite such developments, the rapid growth in trade with emerging economies in recent years has not led to a significant change in the structural pattern of Africa’s trade. Raw materials, particularly oil and minerals, still dominate, as they did 10 years ago. As a result, just a few major producers dominate the continent’s trade with the new markets. Algeria, Angola, Nigeria and South Africa between them accounted for 82 per cent of Brazil’s imports from Africa in 2007 and 53 per cent of China’s, according to the OSAA report. Just 10 countries accounted for 79 per cent of the continent’s entire trade with China last year, the Centre for Chinese Studies reports (see table below).

China’s trade with Africa has been dominated by its desire to secure long-term supplies of strategic inputs, particularly oil and minerals, to fuel its economic development. The Chinese authorities want to increase the share of oil imports sourced from Africa to 40 per cent, from the current 30 per cent. They are seeking to do this mainly through “natural-resources-for-infrastructure” arrangements. In these, African governments agree to long-term supply contracts in exchange for loans to finance the construction (usually by Chinese companies) of related or other infrastructure.

In Angola, China has secured oil supplies in exchange for some $5 bn in loans and other investments to develop everything from houses and farms to ports and railways. China now takes 30 per cent of Angola’s oil exports.

Guinea and Gabon have struck similar deals to supply iron ore and Sudan to provide oil. China now takes 60 per cent of Sudan’s output. The Democratic Republic of the Congo (DRC) has negotiated a $9 bn deal to exchange copper and cobalt for the development of a new mine, plus a wide range of infrastructural development.

Controversy and uncertainty

Recently a number of such arrangements have run into obstacles. The DRC deal has been criticized by the IMF on the grounds that it may deepen the country’s already near-intolerable debt burden (see page). In Gabon the $3 bn Belinga iron ore project has sparked protests by local environmental groups.

In Nigeria a number of projects involving Chinese, Russian, Indian and South Korean financing and companies have been delayed, either as a result of the government’s review of major infrastructure and oil deals or because of the global economic downturn. One of the Chinese projects affected is the $1.6 bn Mambilla hydroelectric dam, to be built in return for operating rights in four oil blocks. That hydro scheme and another in Guinea that is also in question account for 60 per cent of the planned expansion in African power generation to be undertaken by Chinese companies.

These problems come against a background of criticism of the trade and investment practices of some emerging market countries. The announcement of the contract for the Luanshya mine in Zambia obtained by China’s NFC brought protests by the main opposition party, which pointed to a history of labour problems at another copper mine run by the NFC, where a number of miners were killed in an explosion in 2006.

A 2005 study of construction companies in Tanzania by the International Labour Organization pointed to concerns over employment conditions in Chinese companies. Indian, Malaysian and South Korean companies have been criticized in Zambia, Lesotho and Namibia for the sudden closure of factories when earnings on exports failed to live up to expectations.

In addition, a number of non-governmental organizations and others have called on China and other emerging-market investors to refrain from major financial dealings in countries with authoritarian governments or widespread human rights abuses.

Reinforcing dependency?

A number of observers, often from the West, have argued that the long-term raw-materials-for-infrastructure deals in particular threaten to reinforce Africa’s dependency on commodities. Such arrangements are also said to have a poor long-term return, since they do little to generate local jobs or bring in new technologies.

China in turn has accused its Western critics of hypocrisy. But at the same time, it is taking steps to change some of its most criticized practices. The managers of the Kilamba Kiaxi project in Angola are making extensive efforts to hire and train local labour. The DRC deal includes commitments concerning local employment and training, as well as using local suppliers for inputs. The Chinese government has recently issued “good corporate citizen” guidelines to govern the operations of its companies overseas.

According to Kwesi Kwaa Prah, an academic from Ghana, China’s approach to Africa has been mainly positive. But to help overcome the differences that are bound to emerge in such complex relationships, both China and Africa need to pay more attention to “people-to-people relations.”

The OSAA report urges emerging country governments to recognize that their long-term access to Africa’s natural resources depends on developing non-exploitative, “win-win” outcomes. “Every effort should be made to avoid Africa entering a new realm and era of debt dependency,” argues the report.

New money and flexibility

Mr. Davies of South Africa believes that such arrangements can be mutually beneficial. The very lack of detail that has led critics to challenge the transparency of some of China’s deals provides the kind of flexibility such long-term arrangements need to adjust to changing circumstances, he argues. He points to the recent renegotiation of Angola’s oil-for-infrastructure arrangements with China, as well as ongoing discussions on the DRC deal.

China is not the only source of new money. Brazil’s oil giant, Petrobras, has projected that it will invest more than $2 bn in Angola and Nigeria over the next five years, while its steel-producing compatriot, Vale, is putting a reported $1.3 bn into developing coal deposits in Mozambique, where Coal India also has acquired mining rights. India’s Tata is planning a major expansion in South Africa and a number of other countries. Meanwhile, Russia’s Gasprom is looking to invest in natural gas in Nigeria and to acquire oil concessions in Algeria and Libya. Malaysia’s Petronas is a significant presence in the oil sector in Egypt and Sudan.

Farm schemes

Outside mining, Malaysia’s Sime Darby has recently struck a deal worth $800 mn to revive the Guthrie plantation in Liberia to develop rubber and palm oil. Singapore’s Wilmar International has taken a stake in a palm oil venture in Côte d’Ivoire.

More controversial has been the interest shown by some emerging economies — as well as by Western companies — in securing needed food supplies by acquiring large tracts of African land to grow maize, wheat and other food crops. Sudan and Egypt have seen significant amounts of such investment from Saudi Arabia and the United Arab Emirates, among others. China has largely refrained from investing in food, but has shown interest in commercial crops. It has already launched a major scheme in Zambia to purchase cotton from farmers and is reportedly negotiating a similar scheme for jatropha, a plant whose oil can be used for biofuel production.

To maximize their leverage, African governments must better analyze emerging-market trends and develop a strategic focus, argues the UN Office of the Special Adviser on Africa."

But in Africa foreign leasing of large tracts of land can be a very sensitive topic. In Madagascar, opposition to a deal for the acquisition of 1.3 mn hectares to grow maize and palm oil by South Korea’s Daewoo featured as one of numerous complaints by protesters against former President Marc Ravalomanana, who was ousted in March.

Such controversies aside, the agricultural technologies developed in many emerging countries can be valuable elements in their trade and investment deals with Africa, Professor Raphael Kaplinsky, one of the principal authors of the OSAA report, told Africa Renewal.

Ghana has just approved a $40 mn deal with a company in Brazil to help develop the sheanut sector, including by constructing a processing plant and providing relevant technology. Benin, Burkina Faso, Chad and Mali have a similar deal with Brazil to help improve their cotton sector. Brazil’s development of ethanol and other renewable energy technology also presents a potential area for expanding economic links. In addition, Prof. Kaplinsky points to the development in China and India of cheap drugs to combat tropical diseases, which can also benefit Africa.

The Africa Progress Panel, an advocacy group, also sees such synergies. The development experiences of emerging markets in areas such as food security, health, education and cash-transfer programmes puts them in a unique position to support the achievement of the Millennium Development Goals, adopted by world leaders in 2000, the group’s 2009 Annual Report argues.

Maximizing Africa’s opportunities

Africa’s growing relations with emerging economies offer both opportunities and risks.

In a May editorial, Namibia’s New Era newspaper observed that China and India “have developed new paradigms of engagement and have raised the competitive equation with the West in Africa.” Africa must not hesitate to seek favourable terms for such economic deals, New Era argues. But, it asked, “Do we know how to get what we want?”

The growth in economic ties with China and other emerging economies has prompted renewed competitive interest from Western companies in Africa’s natural riches, which can provide African governments with greater leverage. As the OSAA report points out, the DRC’s potential deal with China was also a catalyst for improvements in a number of existing mining deals with Western companies.

At the same time, emerging economies can also compete with Africa, as underlined by China’s recent $10 bn deal with Brazil for oil. The flooding of European and US markets with Chinese and Indian clothing following the removal of market barriers against them led to a 25 per cent fall in African clothing exports, the OSAA report points out.

While Africa’s aid, trade and investment relations with emerging markets can reflect a “win-win” situation, they can also have “win-lose” outcomes, the OSAA report warns. To maximize their leverage, it recommends, African governments must better analyze emerging-market trends and develop a strategic focus. In particular, it urges African governments to work together to develop a regional approach and thus ensure the best possible deals.

The fact that African negotiators must deal with a wide range of entities only reinforces the importance of such an approach, says Prof. Kaplinsky, who notes that there are four types of players in China alone: central state enterprises, provincial enterprises, private companies and small-scale entrepreneurs, each with differing interests.

Prof. Kaplinsky also stresses the need to avoid “wars of incentives” in which purchasers of African commodities play African countries off against each other. In its major trade and investment deals China has focused on bilateral arrangements, and has not so far been a significant factor in the $8 bn infrastructure plan of the New Partnership for Africa’s Development (NEPAD) adopted by African leaders in 2001.

The OSAA report stresses that African countries, through regional groupings such as the Southern African Development Community and the Economic Community of West African States, could present a common front to potential investors and buyers and thereby maximize the potential of emerging markets to meet the continent’s strategic goals. At the same time, the African Development Bank and the UN can help provide African countries with market intelligence and other assistance.

More from Africa Renewal

Podcast