Dialing for cash: mobile transfers expand banking

Dialing for cash: mobile transfers expand banking

In Africa, cross-border remittances by phone overcome bank limits

From Africa Renewal:

Associated Press / Sayyid Abdul Azim

Customers at an M-Pesa counter in Nairobi receiving assistance in making a money transfer by phone.

Customers at an M-Pesa counter in Nairobi receiving assistance in making a money transfer by phone.Photograph: Associated Press / Sayyid Abdul Azim

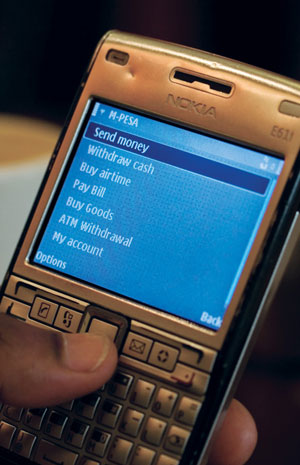

More people in Africa’s poorest countries have mobile phones than have bank accounts. That reality is spurring mobile service companies to explore how they can capture a share of the potential banking market by enabling migrants from these countries to transfer funds back home to their families.

Sending such remittances by mobile phone can be a cheap, efficient and safe alternative to the usual channels of employing money transfer companies or acquaintances traveling to the home country [see Africa Renewal, October 2005]. Money can be sent to even remote rural areas quickly, so long as the recipient has cell phone access or can go to a participating business that pays out cash.

The market is a potentially lucrative one, Pieter Verkade, an executive at the MTN telecommunications company, told Africa Renewal. Such transfers already are “a well-beaten track, with a lot of migrant remittance money coming into Africa for some time through other channels.”

The technology is taking hold especially in countries where established transfer services charge high fees. Kenya’s Safaricom and the UK telecommunications firm Vodafone blazed the trail in 2007 when they launched M-Pesa (M for “mobile” and pesa meaning “money” in KiSwahili). Initially just a domestic mobile money service operating in Kenya alone, it has since expanded into an international transfer service for migrants in the UK sending money home to Kenya. Growth of mobile money services in the Kenyan market, where M-Pesa is still the predominant player, has been rapid. By the end of 2010, four mobile phone operators had signed up more than 15.4 million subscribers — more than half of Kenya’s adult population — to their mobile money transfer services.

Ignored at first

M-Pesa’s rapid growth is particularly astonishing since the service was, at first, “virtually ignored by the financial institutions,” recalls Bernard Matthewman, chief executive of Paynet, which developed software for M-Pesa that allows cardless transactions at ATMs.

Part of the early challenge in launching the service, says Mr. Matthewman, was convincing banks that people outside major cities were potential customers. “Most importantly, in launching the Paynet cardless ATM service, we had to have an education campaign,” Matthewman explains.

There was no reference point for this kind of service. Many of the people M-Pesa hoped would sign up had never used an ATM before, let alone used an ATM without a card. But a cardless ATM transaction can be very straightforward, requiring just a PIN code that is texted to the user and kept active for only a few hours to safeguard the security of the transaction.

In the short time since the launch of M-Pesa, some $100 million has been withdrawn by remittance recipients from PesaPoint ATMs, without the need for bank cards or bank accounts.

Teaming up

The use of mobile money transfers for remittances and small payments, such as school fees and utility bills, has expanded beyond Kenya to other African countries. In South Africa, Vodacom recently teamed up with Nedbank to offer the service for domestic transfers. “Vodacom’s existing penetration into the target market — its distribution coverage through outlets even in rural areas — was attractive to us,” says Ilze Wagener, an executive at Nedbank.

Mobile money transactions can offer banks a way to reach people in rural markets without the expense of building new branch offices or agency outlets. By May 2011, nine months after its launch, the Vodacom-Nedbank partnership had signed up 140,000 customers in South Africa and set up more than 3,000 M-Pesa outlets and 2,000 ATMs throughout the country. In a country like South Africa, which has people both with and without bank accounts, as well as a range of retailers from very sophisticated to simple, “we have to think about M-Pesa in a very different way,” adds Ms. Wagener. The service “has its own unique set of new opportunities and challenges.”

In some countries, banks are forming partnerships with multiple telecommunications companies. “The mobile money network we now have in place, through partnerships with four different telecoms companies in Ghana, has enabled us to extend our services to reach customers in every part of the country,” Owureku Osare, Ecobank’s head of transaction banking in Ghana, told Africa Renewal. Mr. Osare described Ecobank’s development of a mobile money network throughout Ghana as part of a larger strategy to build up the bank’s client base.

Mobile banking services, such as M-Pesa in Kenya, make it easy for people without bank accounts to receive remittance payments from relatives abroad.

Mobile banking services, such as M-Pesa in Kenya, make it easy for people without bank accounts to receive remittance payments from relatives abroad.Photograph: Africa Media Online / Felix Masi

Reaching the 'unbanked'

There are increasing signs that traditional banking and other financial services are adapting to this new technology and new market in ways that increase financial access for those without bank accounts, the “unbanked.” Banks offering mobile money services are encouraging people who may have some money left over from remittances to hold it in “mobile wallets,” basic electronic accounts linked to a mobile phone.

“By making it easy for unbanked people to hold money in the mobile wallets linked to their mobile phone numbers, the hope is that eventually the money will find itself in an actual bank account,” explains Mr. Osare. In May, Ecobank introduced a mobile savings account that can be linked to a mobile wallet for customers in West Africa.

M-Pesa also provides an interesting case. Last year it formed one of the first partnerships in which a telecoms company and bank teamed up to offer a basic interest-earning savings account, known as the M-Kesho M-Pesa Equity Account. By mobile phone, an M-Pesa user can move money from an M-Pesa mobile wallet to an interest-bearing electronic M-Kesho account, held with Equity Bank.

According to a 2010 report by the Bill and Melinda Gates Foundation, M-Kesho attracted 455,000 new account holders within its first three months, taking off at a faster rate than the M-Pesa service itself had in its earliest stages. In addition to providing a full virtual account managed from a user’s cell phone, M-Pesa offers the M-Kesho account holder the opportunity to take out a microloan after several months.

From insurance to 'cash-lite'

Beyond savings accounts and microloans, banks have also begun introducing prepaid debit cards and insurance services to this new market. Insurance policies that cover funeral costs are now an important financial service in many African markets, but so far they have usually been confined to cities, according to MTN’s Mr. Verkade.

With mobile money transactions catching on rapidly in Ghana, Hollard Insurance and Mobile Financial Services Africa joined with MTN in early 2011 to launch mi-Life, a mobile “micro-insurance” service available by mobile phone. “These insurance services make complete use of our technology, so that the entire registration process also happens over the mobile phone,” Mr. Verkade explains. With very small premiums, the idea is first to tap into the strong unmet demand for this kind of service in Ghana, including in underserved rural areas, and then to extend the service to other African markets, such as Rwanda.

Partnerships between telecoms firms and banks and other financial service providers can be expected to increase, to serve a rising number of African countries and markets.

Another logical step is to move more in the direction of “cash-lite” — transactions that eliminate or greatly reduce cash in the money transfer system, says Mr. Matthewman. “We’re beginning to see that already, where you can buy your prepaid airtime on an M-Pesa phone and send the airtime to another phone user, eliminating the need for paying in cash.” In that way, a remittance sender could send prepaid airtime to a recipient, who in turn could exchange the airtime directly for goods or services at participating retail shops.

For mobile transfers, headaches remain

Despite the rapid takeoff of cross-border money transfer services by mobile phone, companies providing them face a number of difficulties. These include:

Existing market conditions: One factor in the rapid growth of M-Pesa in Kenya was that when Safaricom introduced it, the company was able to capitalize on its near-monopoly position in Kenya’s telecommunications market, which gave it a high level of brand awareness. But M-Pesa and other telecoms services have not been able to replicate such rapid growth in some other markets.

Liquidity: In more remote, rural areas, money transfer services may not always have enough cash on hand to pay out to people receiving remittances. To deal with the problem, Owureku Osare of Ecobank in Ghana says that his bank is looking at partnering “with a microfinance institution that already understands that terrain to get the liquidity support to the agents in these areas.” In Kenya, Paynet’s system of using cardless ATM transactions offers another solution.

Mistrust and unfamiliarity: Many rural inhabitants mistrust or have no access to banks, and are therefore not accustomed to using them. But taking advantage of the wide popularity of mobile phones, some banks and telecoms providers are literally taking their show on the road, sending staff from town to town in even the most remote rural areas to demonstrate how mobile money transfers work. Others train local spokespeople, who earn commissions for signing up customers.

Technical obstacles: Although Ecobank in Ghana operates in 30 African countries, it has not yet been able to find a telecoms company with a single platform hub that would enable the bank to provide mobile money services across national borders.

Varied national regulations: Laws and regulations for sending small cross-border payments vary by country and can be unclear about sending such payments by mobile phone. Kenya’s central bank is currently developing draft regulations for electronic money issuers and electronic retail transfers, and Tanzania’s central bank has also announced that it is preparing a new draft law to regulate such transactions.

Monitoring: In South Africa, mobile money transfers are so far available only within the country, and all cross-border transactions, even very small ones, must be monitored. Under the country’s anti-money-laundering law, only banks and other authorized dealers may carry out cross-border money transfers. This excludes retailers, which are a core part of the banks’ mobile money strategy in the domestic market. Meanwhile, the banks themselves are reluctant to engage in multiple small cross-border transactions because it can be costly to report them to regulators.

Podcast